When I heard that Flipkart had raised ANOTHER 200Mn US$ round in financing, my body went through hormonal changes. I was amazed at the strength of the Flipkart team and their business traction to raise such a massive sum; yet my calculative Marwari brain went a bit haywire.

I promised to write an UNBIASED view on the same, and while thinking of the approach remembered the Doodhwala (Milkman) who used to deliver milk at home. That bugger was a cunning guy – who would always “mix” pure milk with water; which made my Granny fret all day. In the end, he sold, we bought and what we drank was a heavenly mix of doodh and paani!

In this case, let me deliver the Flipkart funding story to you as reported in this media article and even separate the Doodh and the Paani (milk and water) for you. Then you decide what proportion of the story you want to buy!

Bansal said, “This investment validates the belief that our investors have, not only in our capabilities as a market leader, but also in the potential of e-commerce in India.”

Doodh part: There is no doubt that the existing/new investors of Flipkart have amazing faith in the existing team and hence have pumped in an additional 200Mn US$. No one manages to raise such large of amounts without ‘faith’. Bravo!

Paani part: I know of a very large Indian Industrial Group that had borrowed between 3-4 Billion US$ from ICICI, IDBI, etc in the mid 90s to build all kinds of ‘plants’ and ‘projects’ in India. The markets turned sour and the investors became cagey and very demanding. They refused to lend more monies to the promoters and demanded profitability from the projects, etc, etc.

One day, the promoter group CEO made a set of ‘mock keys’ and went to meet the investors. He told them, “Sorry, I am not able to run these businesses. Please take these keys of the plants and do as you please.”

The investors GOT THE MESSAGE. He was saying, “Either lend me more money or lose all the 3-4 Billion you have given me so far.” They lent more, and today that group is amongst India’s top 20!

I personally don’t know if the ‘existing’ investors of Flipkart are participating out of pain or pleasure. But given that Flipkart has already raised 180 million US$ in the past, investors are not really in a position to ‘write off the money’ as they would do if they would have invested 10-20 million US$ in small and medium companies.

Bansal: “We will use money to build the technology platform, further grow the supply chain besides talent acquisition.”

Doodh part: That sounds like a nice ‘PR’ statement, although I wonder why would ‘talent acquisition’ be mentioned here. I mean who raises 1200 crores in part to HIRE PEOPLE? Who the heck are these people? All the Fortune 500 CEOs???

Paani part: Let’s examine the current business of Flipkart. I see three companies in one:

– A courier company that only fulfills orders. This requires investments in warehouses, staff, vehicles, and yes, lots of technology to manage back-end. Let’s assume that the best business in this category is DHL.

– A Walmart-like purchase powerhouse that has the ability to BUY goods cheaply and then sell them expensively to consumers. The cheaper the purchase and more expensive the sale, the better the margins.

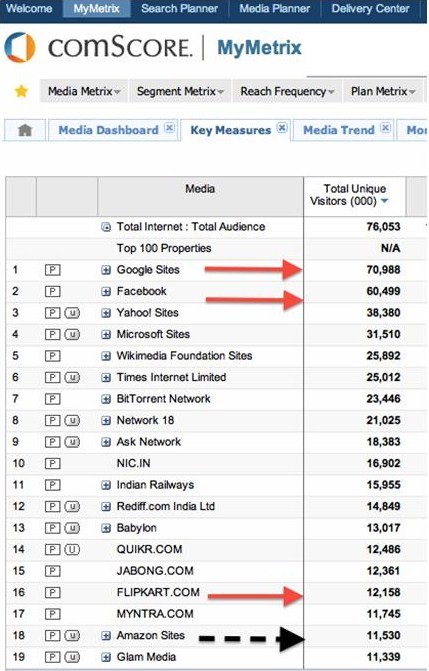

– A consumer Internet brand that has to grow popular each month and keep attracted to it by any means, with minimum advertising (advertising just for traffic becomes unviable). In this league, facebook and google come to mind. (A comScore Top India Internet sites chart is produced later).

So, in effect, Flipkart is going to try and become a better DHL, Walmart and Facebook all at once??

I think that is a really tough job!

Bansal said, “The company has already achieved half of its target of $1 billion GMV (Gross Merchant Volume) by 2015. We can be profitable even today if we want, but it is a strategic decision not to, as of now.”

Doodh part: It’s gratifying to know that at least the massive investments of the past (180 million = 1000 crores (excluding this one)) have at least resulted in a ‘break even business’!

Paani Part: ‘Just about profitable’ finds no meaning on any market of the world. You have to be Supercalifragilisticexpialidociously profitable to make any mark OR show some other promise to the market to be valued very high – as in the case MakeMyTrip who projects itself as the default leader of Travel in India/ (see MakeMyTrips market cap here despite it making a loss).

As per Bansal’s statement, as on today, Flipkart does 50% of 1 billion in GMV (Gross Merchandise Volume). That means that Flipkart does 500 million US$ = 3000 crores in Gross Revenues. If the company becomes ‘just profitable’ at this level of operations, let’s assume that the profit will be 5% = 150 crores = 25 million US$)

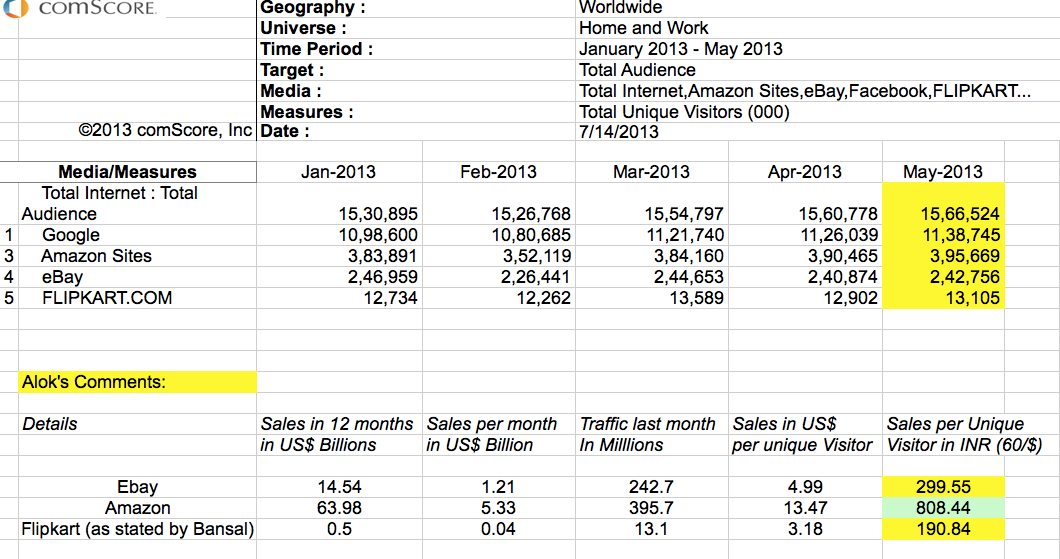

Now, check out this chart of market caps of ebay and Amazon – dated 13.07.13 and pay attention to the red arrows

Given the assumptions made on Bansal’s comments, in the USA stock markets, Flipkart would be valued best at 1.00 – 2.5 BN US$ (assuming 2-5x multiple on sales and/ or a 50-100x PE!)

Wow? Let’s consider the capital table of Flipkart post this round. Reports say that the VCs now own more than 50% of the Company.

Hence 380 million of investments have bought VCs 50% of Flipkart.

To get back a classic 10x on investment (=4 billion US$), Flipkart will have to sell or list at 7-8 BILLION US$ for its VCs to earn a 10x return on the same!!

(Side comment – even a 2.5 billion listing will result in VCs getting back 1.25 billion or 3-4x on their moneys. Nothing great in multiples, but definitely a BIG exit on a BIG investment and something that everyone would term a big success).

Bansal said, “The company has currently 9.6 million registered users and over 1 million unique visitors a day; it achieved a peak of 130,000 items shipped in a deal last month.”

Doodh part: 1 million daily unique visitors in India is GREAT. That’s no mean feat given that the top media Internet leaders are the usual biggies!

Check out this chart of Monthly Uniques of India (comScore May 2013)

Paani Part: CHECK OUT the AMAZON site’s traffic in India and how CLOSE it has crept up to Flipkart!

A haunting question I have is, “What is the COST of acquisition of the traffic of Flipkart?” If you look at the chart, Quikr.com is higher than Flipkart.com in May 2013. That is clearly from their relentless advertising. What would Flipkart’s traffic be without advertising?

Now, for the KILLER 🙂

Check out THIS comScore traffic chart juxtaposed with the Market Cap data:

(note that the Internet traffic of Flipkart here is slightly higher since this is a global traffic chart):

The chart tells an interesting story…

Consider ARPUU’s (Average Revenue per Unique User):

Flipkart seems to be selling goods worth Rs. 190/- per unique visitor – a bit under ebay.com’s global ARPUU of Rs. 299/- ; BUT AMAZON ARPUU is a stratospheric Rs. 808/- per user!

If Flipkart has to become a Company double its size (1 billion US$ in revenues), it will have to double its traffic, which will then equal to the Times of India Group’s monthly traffic. To achieve this scale of traffic without expensive (and unprofitable) advertising will be very difficult. Else, it will HAVE TO INCREASE its ARPUU significantly.

Bansal: “This will not only enable us to reach our goal of $1 billion GMV by 2015 but also help us achieve bigger milestones in the future.” In April this year, the firm launched its marketplace and integrated it with its existing e-commerce platform to enable third party sellers to list and sell their products on its website and sell directly to consumers. The firm claims to have over 500 suppliers on the marketplace as of now.

Doodh part: Flipkart has done a GREAT job. They are the ‘e-commerce’ destination that every Indian I know uses and continues to use. Also, honestly, the brand is now so strongly entrenched, that it’s going to be difficult for the other ‘Chunnu Munnus’ of e-com in India to catch up. They will soon be cremated, buried or given to the birds (based on their preference).

Paani part: The challenge IS NOT FROM INDIA, BOSS!

IT’S FROM THIS MAMMONTH, GAMMOTH ANACONDA CALLED AMAZON!

This is the Corporate Vision of Amazon as it reads on their site. Just check its audacity: “We seek to be Earth’s most customer-centric company for four primary customer sets: consumers, sellers, enterprises, and content creators.”

!!!

If you get a few minutes, download and read this letter to shareholders Bezos wrote for 2012.

A few sentences to drive my later points:

– Prime Instant Video selection tripled in just over a year to more than 38,000 movies and TV episodes

– One industry observer recently received an automated email from us that said, “We noticed that you experienced poor video playback while watching the following rental on Amazon Video On Demand: Casablanca. We’re sorry for the inconvenience and have issued you a refund for the following amount: $2.99. We hope to see you again soon.” Surprised by the proactive refund, he ended up writing about the experience: “Amazon ‘noticed that I experienced poor video playback…’ And they decided to give me a refund because of that? Wow…Talk about putting customers first.”

– I am happy to report that I recently saw many Kindles in use at a Florida beach. There are five generations of Kindle, and I believe I saw every generation in use except for the first. Our business approach is to sell premium hardware at roughly break-even prices. We want to make money when people use our devices – not when people buy our devices. We think this aligns us better with customers. For example, we don’t need our customers to be on the upgrade treadmill. We can be very happy to see people still using four-year-old Kindles!

In 2013, Amazon is NOT the ‘e-commerce’ Company that Flipkart is trying to compete with (or will be forced to compete with)! That was the Amazon of 2005!!

Amazon TODAY is another PLANET.

Why do I say this?

Consider the points I mentioned about what comprises Flipkart – Courier & Logistics, Purchasing Power & Web presence & brand.

What comprises Amazon today?

Its CONTENT meets DEVICES meets DISTRIBUTION – all done seamlessly and as evident from anyone who has experienced Amazon before.

Amazon is the ONLY company that has succeeded in really successfully merging hardware (Kindle) and software (all kinds of content), beyond Apple Inc.

Jeff Bezos is NOT fighting the “Let me buy books cheap and then send them to Austin via my own expensive courier just to deliver it to Alokbhai there to make him happy.”

Nope. Bezos has MADE Alokbhai BUY a Kindle on which he BUYS books (that are severely discounted) and which INSTANTLY get delivered!! There is no blue dressed courier calling 10 times to find which galli Alokbhai lives in. No COD, no lafda, no problem.

Just before I end, let me quote a few lines from this epic article in Business Insider on Amazon and the Kindle:

- Amazon’s Kindle is no longer just a product: It’s a whole ecosystem.Specifically, it’s not just an e-book reader but a tablet, a media store, a platform for digital media sales, and even a publishing imprint.

- Media (means non physical stuff) is 45% of Amazon’s revenue, and it is in the midst of a secular disruption as physical media is replaced by digital media – (this tells you what the future is about!)

- Right now, Amazon generates 45% of its revenue from the sales of physical media–books printed on dead trees, DVDs and the likes. This form of media distribution is, slowly but surely, going the way of the dodo bird (or at least the tiger). No one knows when, no one knows how, but it’s happening.

- Amazon has to lead that disruption, instead of being disrupted by it. Books are a great example. With the original Kindle, Amazon pioneered the sale of digital books, and as a result owns over 90% of their distribution.

- Kindle is a decade-long investment in a media consumption and distribution ecosystem. It’s something Amazon can’t afford not to do because it needs to disrupt itself.

I am excluding all the existing business that Amazon does currently in India via its Market Place model of amazon.in (which Flipkart has also started). That’s all stupid distraction and will disappear when FDI is opened up, etc, etc.

I think the killer is going to be instant gratification of goods bought on platforms that are OPERATED BY e-commerce giants – NOT ‘via-via-via-via-via.’

Apple TV, Kindle and the Kindle App soon to be available on ALL Android Tabs and Phones in India is what will be Flipkart’s nightmare. That’s what they have to watch out for.

Can Flipkart create their own tab and platform like Amazon and iTunes/Apple?

Or most critically, as Business Insider puts it – Can Flipkart Disrupt itself when the time comes?!!

That my friend is the real adulterated question you need to separate into doodh and paani!

Your faithful doodhwala,

*****

Many thanks to Sumesh for the doodhwala image!!!

Sahil

nicely written and interestingly magnified Alok. But i am not yet convinced about the fact all going behind Flipkart. No one’s appreciating the fact that ‘Bansals are the man behind todays INDIAN e-com’ and they have given much before they started making it.

I believe its like ‘Agar log tumhari baate kar rahe hai to lagta hai tum Tarakki kar rahe ho’

Never Mind – You have proved yourself as nice calculator and financial magnifier . Loved it – keep em coming

Mansi Bhambhani

Excellent Piece. The Analysis on every aspect is too good

Alok Rodinhood Kejriwal

?? I am in awe of them! Sorry if you think I am running them down. Seems you didn’t even read the piece!

Check comments like:

– There is no doubt that the existing/new investors of Flipkart have amazing faith in the existing team and hence have pumped in an additional 200US$. No one manages to raise such large of amounts without ‘faith’. Bravo!

– 1 million daily unique visitors in India is GREAT. That’s no mean feat given that the top media Internet leaders are the usual biggies!

– Flipkart has done a GREAT job. They are the ‘e-commerce’ destination that every Indian I know uses and continues to use. Also, honestly, the brand is now so strongly entrenched, that it’s going to be difficult for the other ‘Chunnu Munnus’ of e-com in India to catch up. They will soon be cremated, buried or given to the birds (based on their preference).

Sorry if you are biased even while pretending to be unbiased!

–

Saraswathi Pulluru

Excellent article. I agree with you Alok – although what Flipkart has achieved is enormous, once Amazon enters the picture – the entire competition landscape changes. For that, they need not spend part of 1200 crores to hire people – but they could spend a major part to see how then can survive and beat the competition!

Vishesh Khurana

good one Alok good read.

Nameet Potnis

Excellent analysis.

Besos is in another league because of the way he think, plans and executes! Read below, this is what differentiates him from the others!

Also, I dont know if you managed to read Mahesh’s rough analysis of Flipkart and their revenue estimates. Pasting it below and will also put a link to the original below the pasted version:

Read Quote of Mahesh Murthy’s answer to Flipkart: As per the news Flipkart has raised another round of funding ( $200 mil ) from MIH and Tiger Global. Any idea how much equity the founders own in the company after 4 rounds of fund raising? on Quora

Once again, thanks for making the doodh ka doodh 🙂

Garima Kaushik

Very Interesting! 🙂

I hope flipkart doesn’t lose their focus, as they seem to be doing lot of stuff, specially with their new PG.

You’ve gone to the length of adding a pic supporting the title of your article, nice touch!!

Harsh Jain

Totally agree that Amazon will simply outclass Flipkart in the end. I’m a loyal amazon fan, and especially love their Prime offering

Manoj Nair

Alok, I had posted a news article on my LinkedIn that talked about the USD 200 million infusion. Do you think they are just setting themselves up to be acquired by Amazon? It’s hard to believe they are ever going to stand up to any kind of competition from Amazon…I don’t think Amazon needs Flipkart (although it would help entering the physical and complicated world of Indian distribution and its not bad to inherit the mind share Flipkart has in this country). I think Flipkart (or the investors, more critically) needs Amazon.

Swapnil Nadkar

Hi Alok…great article…just a small request…can you please provide the link to the Business Insider article you refer to, its missing. I tried searching for the correct article but was not sure which one it was…Thank you.

Ajaz Siddiqui

Mind blowing analysis. I have been waiting desperately for this one; even thought of asking you about it, and FINALLY here it comes. The wait was definitely worth it. YOU ROCK ALOK!!!

Alok Rodinhood Kejriwal

Thanks – added it it to the link and also here – https://www.businessinsider.com/kindle-economics-2011-10

Sandesh Kumar

Awesome article.. superb!

harpreet singh

Thanks Alok, Beautifully analysed,

You have placed their positives and negatives in view , for people to take their own call

and yes , as i expected, the negatives are huge , clearly as they need large amounts of capital to keep it going. The Godzilla Amazon is already here & expanding

The investors have become the owners 😉 by virtue of them owning > 51% so now they are infusing capital as its their own company but will they put in that much capital needed to compete & outwit Amazon , i dont think so this will ever happen

these infusions , though large by indian standards arent enough to make Flipkart get that edge

so net net either Flipkart will be an average investment / business just about in black guzzling enormous amounts of money to stay afloat ( an extra large IPO , if market allows, may give them some decent financial muscle )

or despite its achievements, it will be a spectacular failure, sometime down the road

In the end its not about an ecosystem , a pioneer status or any such credo but only about making money !

thanks again !!

Bansi Kotecha

Very well written and analysed….completely agree on the point “

In 2013, Amazon is NOT the ‘e-commerce’ Company that Flipkart is trying to compete with (or will be forced to compete with)! That was the Amazon of 2005!!

on some levels i think they are just setting the stage for Amazon to enter India and acquire them…

Harmanjit Singh

WOW! Really enjoyed reading your analysis!! Very informative.

Alex J V

Awesome article. Puts a lot of things in perspective.

I was wondering how can we get access to comscore? Is there a free part? If so can you write an article on how to use it? It looks like it is accessible only for enterprises ..

Alok Rodinhood Kejriwal

yeah – it costs 1.5 lacs a month 🙁

Alex J V

Wooo … I am speechless !!

Regarding market research and estimating size of market – is there any other data source (“free” 🙂 ) other than google adwords and facebook ads api?

Jolly Mathur

Excellent analysis it has given me lot of gyan for my second round of funding…

Jitin Pillai

Excellent analysis Alok! Enjoyed every bit of this.

I used to look upto this company a lot in its early days. I really wish Flipkart focus on their execution and get their act right, there is nothing that cant be done even in wake of huge competition. Here are few points that I feel might help them –

1. Get their PR right. If they were once the darlings of Indian Startup Ecosystem, then they should capitalise it. Help some other Indian companies (atleast using their products & even promoting it). Build an ecosystem, get bunch of people behind them to rally. (Tweets & FB references will get you more than TV ads, in my opinion)

2. Pay your vendors on time (against the delay which extends beyond months). Keep them happy, you will have the most imp people who will want you to remain in business. And they might go miles.

3. Have a core value, something that you stand for (other than selling stuff). If you have one, yell it to others. Today no-one knows what is FlipKart stands for. (eg – I love Apple not for their flashy gadgets, but for something more, something deep. And I will still stay with them even when I know I can get something better, bigger, colorful, blah-blah at 1/3 of the price). Now this has to be earned, and most cases for customers its hard to let go of this.

Thanks Alok for this article, keep them coming!

Anirudh B Balotiaa

Another great article by the “Yoda” himself! 😉

Was reading an interview post this funding news of the Bansals, where they clearly say that they have no plans on the anvil to go into the hardware business. So if Flipkart wants to build an eco-system which will be inevitable once Amazon comes in fully, they better start now than hurry and make a mediocre product later on.

Also those who want to have a e-reader already have a Kindle or a Kindle app on their tablets. Even if Flipkart does bring out one, until is unless is real real cheap, do you think any current Kindle reader will shift? As scary as it may sound Amazon has a build a SOLID business and they haven’t even entered India completely,

Also I am not a fan of these “seller marketplace” as a consumer. I am not assured of the quality nor the shipping time. Yesterday I was buying something on Flipkart and apparently the seller doesn’t ship to Mumbai!! If they don’t have the resources to ship to Mumbai then I don’t know what they are doing on Flipkart!

What they do with $200 mn of cash is the key for Bansals!

Sidharth Udani

How I wish I could start thinking in a way you have thought about this whole issue. Great article alok. I hope future flipkart makers reads this.. {Applauds)

Afroze

They seem to be setting up for Amazon acquisition, might have received some sort of an indication from Amazon or maybe something else which we are not aware of. Otherwise I wonder why VC’s would invest 200 mn $ to compete against Amazon.

Anirudh B Balotiaa

Yeah seems likely!

Deepak Singhal

I am a big fan of Amazon; but a bigger fan of Flipkart.. Few points I would like to raise here:

1. In India if we raise 200 million ; people think its big money while in US raising 100 million is very trivial. .. Many startups raise that much money. And flipkart being the e-commerce leader of India deserves much better valuations. We should NOT value any highly growth oriented company based on sales or earnings. Giving same financial ratios as Amazon/Walmart to Flipkart is injustice because Flipkart has just started evolving.. Just few years old company but in the right domain and country with right demographics. Growth potential is just exponential.

2. I really dont want Flipkart to get acquired by some Amazon. I agree We couldn’t come up with some great products like Apple, Samsung etc. did but this is our chance to build one such product when we have so many advantages on our competitors ( early move, personal touch with suppliers, knowing market much better than any MNC can )

3. Guys please give some time to Flipkart. Please. Amazon took 15 years to reach here.

4. If some products are good; it can easily be used worldwide. Not same for e-commerce. Otherwise China would not have such e-commerce companies with huge market cap and revenues.

Samruddha Salvi

This doodhwala seems to have joined the gym… 😉

Govind Kabade

Bravo !!!! , Was reading so many news and article about the deal. But, Bingo, You cleared the air. Thank you. Loved reading the full article and explanation and Best part is Doodh & Pani Comparison

Keep enlighten us.

Cheers

Govind

Haresh Motirale

This was absolute knowledge…thank you so much for sharing the analysis 🙂

kiran n. bolantkodi

Nice to compare it with doodh and pani….Its an eye opener about e commerce. I m a brick and mortar ( in food business) guy and sometimes i’ m so overwhelmed by these e commerce “galata”, i thought of starting one!!! In IT space scaling up is easier but with risk. You are betting on something you cannot see…..we are uncomfortable with that.

Shriram

Well researched article Alok. Appreciate your insights.

However, Flipkart’s main competition is not Amazon and vice-versa. They are all competing with the over 12 million retail outlets across the country. I had written in one of the articles (at http://www.mymilestogo.com) earlier that the death knell for Musicworld which shut down recently was not just piracy – it was because they were not promoting Music as an Industry. Similarly, Flipkart and its likes must promote E-Commerce as an Industry and not just themselves. I recently bought an ADSL Modem from Flipkart after researching quite much offline – the online price was cheaper by Rs. 800/- and obviously I bought it there. Flipkart air lifted the piece from Mumbai and delivered it within 26 hours! Assuming they made 15% Gross Margin on a product price of Rs. 2,300, where is the Net Margin? At this stage,it would be impossible to survive beyond the next 18 months for them.

Vikas

I think this round is done in bit haste to capitalize on rupee depreciation since FK probably already had ~50M cash which should be sufficient for next 6-12 months.

Sanjana Chauhan

Great article. Well researched and detailed.

Only time will tell how Flipkart can compete with Amazon.

Nithya Prabu

Awesome. Great analysis 🙂 your choice of words.. brilliant… special mention: “supercalifragilisticexpialidocious” Smart!

shridharan Ramamurthi

According there can be only two reasons for this kind of investments-1.they have invested to save their existing investment and probably dont want to call it a failure and jeopardise other such investments in an already fragile PE investment scenario in this country.2.The promoters are very good story tellers and like cute babies at night they have listened to it and happily got sold into.

Ketan Warikoo

Dear Alok, Good piece. The numbers and everything are good, giving both sides of the story. I’d just like to present my take.

Something that you really gave credit to Amazon for, i.e. customer centricity is also there in to a certain extent with flipkart. Even if you say they dont have customer centricity (as in a pro-active refund policy), I believe you will agree with me when I say what they are getting is excellent feedback from their customers. Each and every customer review thanks Flipkart for their prompt delivery & packaging (not a very commonly appreciated thing in the Indian market) first and then reviews the product. And then ends the review again with thanking Flipkart! Isnt that kind of crazy considering the Indian consumer is never satisfied with service and finds it hard to thank a retailer from the bottom of his/her heart?! Of course, Amazon is expected to do better if not equal at the very least, so we still have to see how this pans out. But Flipkart did disrupt the normal slow supply chain when they arrived.

Also something that popped in my mind when you did those ARPUU calc, I think the numbers are broken. Simply because the basic cost of several things in Amazon US & UK are simply more than they are in India and a raw conversion from USD to INR doesnt reflect well on the situation. Case in point, books in India are around 250 bucks, while books aborad cost minimum of 10 dollars (in fact I think it could be as high as 20 dollars) which gives another story about the margins for the e-retailer. And dont even think of comparing textbooks, the difference is huge! (you remember how India has Low Price Edition?) Not a fair comparison IMO. Likewise with DVDs, hardware items, furnishings, fitness equipment, all such branded things have a high price in dollars.

As for that point about Amazon having its own device, I think the market in India is already really fragmented with so many cheap tablets running android up and about. Not like US/Europe where either people dont have tablets or have Ipad. So India has many ebook readers up and about, just that the question that needs to be asked is do Indians have an ebook reading habit? Maybe they will introduce a device later but right now, all I see is many people with 5″ phones and 10″ tablets that are only being used to play Fruit Ninja! 😉

Otherwise great doodh-paani story!

Cheers!

Alok Rodinhood Kejriwal

Not sure what your CENTRAl argument is ?

– reviews are are all fine, but what happens when FK raises prices to become break even? Will everybody be around to praise them still? or will the same customers have disappeared to other sites and be busy praising them?

– if the sale prices are higher in USA, then costs are higher too 🙂 Also, Amazon operates in 200 countries – not only in the USA. Finally, given that 45% of Amazon sales is digital media, their sales prices are lower not higher 🙂

– I think you rushed up in your last point. Tablets are NOT just e-readers, they are games, music, movies, education, TV shows etc! And to my own point – the more devices get loaded with the Amazon APP ( not necessarily kindle), the worse it becomes for FK!

Ketan Warikoo

Hi Alok,

Thanks for the reply!

– I wasnt posing any central argument. I was just putting up for discussion different perspectives on some of the points you mentioned. As I said your article is really nice! 🙂

– At their current prices, I am not sure they are making losses. They have enough margin on nearly all categories of products. The chunk of the losses should stem for the expansion plans and bringing more areas (less lucrative) under coverage. Of course, I may be wrong. Please feel free to correct! Also they cant raise prices too much since there will always be amazon 😉

– Okay, good point you mention! 45% sales from digital media, so that means the chunk of amazon sale is from stuff that doesnt have a higher basic cost and has high margin in dollars(compared to non-digital stuff which has warehousing, distribution and such costs). And FK has a primarily non-digital presence. Its lopsided and that is owing to the nature of the market. So ARPUU numbers dont convey the real situation I think. A fair comparison would be comparing ARPUU numbers for amazon india and FK, once amazon has spent some time here.

– I did rush up my last point, well caught! It was an afterthought. And that point of yours is very right, amazon has a huge ecosystem that they can just port to india and FK can do nothing about it. Though FK is trying with their wallet and ebook offering (no apps though), they are on a slippery slope given what they are up against! Its just a matter of amazon creating a digital market that can change the way Indian consumers consume (and pay for? :P) content.

Rishi Jasapara

Flipkart now also releases it’s own payment gateway services – PAYZIPPY. Another segment where Flipkart is entering. Check this article of The Hindu. Also Flipkart Marketplace coming up. Lot of things up Flipkart’s sleeves it seems.

Sanjaya Choudhary

The heavy dosage of VC funding goes over my head . Anyway i truly enjoyed the doodh ka dooh aur pani ka pani , great way to disclose the Indian e-com Market. For getting the story in a free flow i will read it again. Enjoyed it.

Alok , Dudhwala se hoshiyar rahna.

Sridhar V

Interesting article on the positives and negatives of Flipkart. The Doodhwala pic looks cool! ha ha.