Have you ever purchased an insurance policy? Actually, wrong question. Let me rephrase: Has an insurance agent ever sold you an insurance policy? Chances are your answer would be in affirmative.

You would have bought it for one of the following reasons: Save tax, invest, get insured, to please the agent because he is your retired uncle or friend or friend’s friend etc or your father bought it circa 1990s. In a country where average insurance amount is abysmally low, the case in point gains even more significance.

Note: By insurance, I mean a traditional policy like endowment, money-back, whole-life, pension etc. These policies cover more than 60% market share today. Other major insurance policy types are ULIPs where the returns are not guaranteed and Term plans, the purest form of life insurance.

So, let’s understand why your policy sucks?

Reason 1: Investment under the garb of insurance

While insurance companies should be selling insurance, unfortunately in India that is not the case. Consider this: The average insurance amount of an insured Indian is just Rs.90,000. What would an average policy holder’s dependants get if he were to die? Rs.90,000. That will not last long.

Insurance needs for a middle income individual having a family of 4 and having modest financial goals would work out to at least a crore. But an insurance company cannot just survive selling term plans, you see. They are low profit products. So they are compelled to sell investment oriented insurance products with high cost structures.

Tip: Go buy a pure term insurance for yourself. Buy an online plan. They are dirt cheap these days.

Reason 2: Negative returns

What if I told you that your insurance policy gives you -2% returns? All this in spite of locking in your money with the insurance company for 20-30 years? Shocking but true. The negative returns are actually net of inflation or in other words real rate of returns. And that’s what counts.

Today the inflation rate hovers around 8-10% and any traditional insurance policy will give you returns in the range of 4-6%. May be 7-8% if the plan is real good.

Tip: If your investment horizon is that long, you are better off parking that money in a PPF if you do not like taking risk and earn 8.8%. Better still; invest in equities where returns over such periods have been in the range of 15-18% tax free.

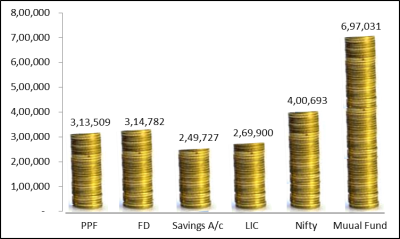

Reproducing a comparison table we had created some time back. The accompanied chart shows the amount you would end up accumulating after investing Rs.20,000 per annum in various investment products for 10 years starting 2002

Let’s decode this: Assuming average inflation was 7% in this period (in reality it was much higher) your savings should have grown to Rs.2,95,000 to just beat inflation. Just check yourself if you have actually become richer or poorer.

Reason 3: Pathetic surrender charges

Ever asked an agent what will be the surrender charge if you ever wish to surrender the policy? It’s a dreaded question and an experienced agent will quickly defend it by saying that the main aim of an insurance policy is to inculcate forced saving habit.

On the other hand similar tax saving products like PPF, ELSS, 5 year fixed deposits have no surrender charges after certain lock in of (3-5 years). Compare this with insurance policy where the surrender charges can be as high as 50% even after 5 years.

Tip: If you have recently purchase a policy and paid 1-2 premiums, just do not pay any more premiums. You won’t get anything back but the opportunity cost is what you need to consider.

Reason 4: Opaque cost structures

In my opinion the biggest reason I hate traditional policies is their opaque cost structures. If you buy or invest in something, shouldn’t you have a right to know how your money is being invested?

A listed company on NSE where you own shares publishes its annual report. In any mutual fund scheme where you invest money you can clearly see where the money gets invested, what are the AMC charges etc. Sorry, not the case with traditional insurance plans.

Tip: Always invest in products that are transparent in the way they work.

Reason 5: Guaranteed benefits are a farce

You are promised all kinds of bonuses like loyalty additions, guaranteed additions, simple reversionary bonus, final additional bonus etc. etc. The problem with such statements is that they are just so irresistible and tempting. But only at Face Value.

The bottom-line remains the net returns you will get. A traditional insurance policy will NEVER EVER give you returns in excess of inflation. Period.

Tip: Do not buy a policy just because of the guarantees provided by the insurance companies.

Reason 6: High commissions

Older insurance companies like LIC that are in business for more than 10 years are allowed to pay commissions as high as 40% of your first year premium, 7.5% for 2nd year and 5% from 3rd year onwards. Which means if you buy a policy that has a premium of say Rs.50,000 then the LIC agent pocketed a cool Rs.20,000 from the first year premium itself!

Ronak Hindocha is the founder of Futurewise, a free and easy way to manage your money online. We will be launching our beta release soon. If you are one of those early adopters you can give us a try. We’d love to hear from you. www.futurewise.co.in.

Vikas Bana

What about real estate (If one could afford), the returns have been real good.

karthik.c

Hi Ronak,

A good post about the insurance domain. Will look into my insurance plans as well. I have got 3 insurance policy in my name.

When I went to futurewise site, it asked me for my email id. Good. I remember registering with the site in September. Since I was not able to find the login page. I was curious to see if I had to give my mail id again. But by mistake, I did not enter any mail id and left the space blank and clicked submit. And it says, thanks for requesting an invite. Should the page not have validation? Thought of sharing this with you. Screenshot attached.

Thanks,

Karthik

Ronak

Vikas – Are you talking about real estate as an investment or primary residence? The answer varies depending on what you say. Having said that, as an investment products it has its pros and cons. Have seen lots of people for whom real estate has proved extremely lucky. On the other you’ve got to deal with ill-liquidity risk, maintenance etc.

Ronak

Karthik…Thanks for bringing that to my notice. Am going to check into that right away.

Vikas Bana

I was thinking in terms of investment, I know many who deals with it as an investment option and have been handsomely rewarded.

Anand Shukla

Hi Ronak,

Congrats.. nice article. I have been following, reading and personally practicing this concept of separating of insurance and investment. I dont have any investment in combo plans 🙂

I think the reason for traditional policies having larger share in market is financial literacy. Explaining this separation of insurance and investment in a traditional policy to a CA friend was a big deal for me. Even if people understand this, taking risk on life’s saving is a big deal for them. Very few will be confident of and even able to achieve the returns more than promised by LIC when they themselves will manage their investments. We can blame little here to instability of capital markets but they are dependent of economy and boom, recession are parts of it.

If you take a deep look, its also controlled to a good extent by policy makers (Govt). Whether they wanna control indian capital markets themselves through sources like LIC or let it free in hands of public through mutual funds or other investing vehicles.

Thanks for sharing.

Anand

PS – m also a Chartered Accountant

Ronak

Thanks Anand,

As you mentioned, financial literacy is yet to get to a respectable level. I myself see so many finance professionals who do not understand basic concepts of personal finance. We hope to address this pain point through our platform.

PS: Thanks for signing up. Will keep you posted when we release our beta version.

Regards

Ronak

rahpar

Excellent article

asha chaudhry

hey ronak…

you might want to check this out 🙂

https://www.therodinhoods.com/forum/topics/december-tees-are-you-gonna-wear-think-do