I would like to thank Yuvraj for some really good questions on investing.

I am putting the answers as a blog so that others can find it easily and comment/question on the same.

Mutual funds vs Index funds.

My pick: Active Mutual Funds (assuming we are discussing Indian funds)

Index Funds imitate a given benchmark index and charge less fees. So the returns are as good as the index. Active funds take calls on stocks and sectors and aim to outperform the index. The alpha generated by active mutual funds, more than compensates for the high fees; that’s why I would prefer them.

In US, the stock markets have matured and generating alpha is not that easy. A fund manager generating 1% annual alpha consistently would rank among the best. However, Indian markets are still emerging. There is a significant scope to generate alpha easily. This is because of the market inefficiencies, emerging sectors, presence of basic indices etc.

Accordingly, you would see a majority of active funds outperforming their benchmarks easily over a period of time.

See this article for more details and data (https://thefundoo.com/welcome/articlepage/31/Active+Funds+Outperform)

What do you think about the real estate market. I personally think its overvalued, but its not slowing down at all. I would like to hear the opinion of an expert.

Frankly, I don’t have a clear view of the same.

The real estate market is very illiquid and is not transparent. I am not active in the sector to be able to bring some deep insights, however, here are my thoughts:

- Real estate prices shall keep going up (though there can be corrections, normalizations and periods of lull)

- There seems to be a lot of black money play in the market. This supports the real estate market even when the chips are down (so even though you see the stock prices of related companies coming down, the house prices are not coming down)

It seems the structure is set in a way that doesn’t let the prices to come down. Had it been a pure demand-supply game, we could have applied economic logic.

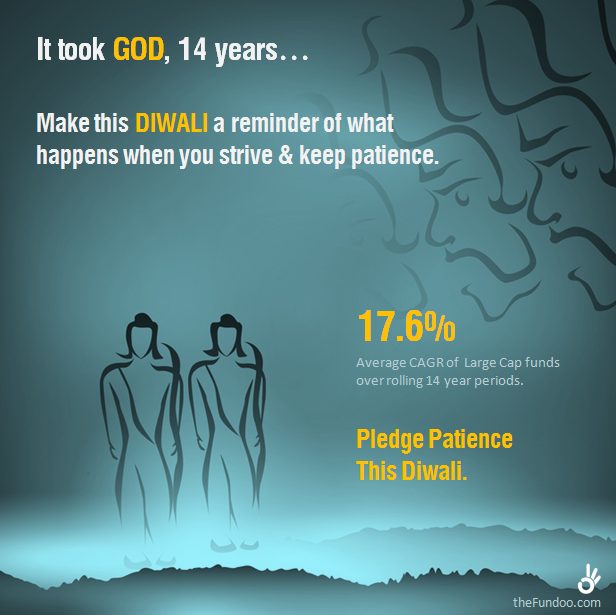

What do you consider the most important skill of an investor.

PATIENCE.

I posted this on last Diwali… (The idea was inspired from Alok bhai’s comments on a facebook post)

Why I say so:

- Investor’s return is often less than the market’s return. This happens because investors get in and/or get out at wrong times. The market volatility drives them to take actions that they should not

- Investor should ideally invest with a time horizon in mind and just sit tight irrespective of what happens in the market during the investment horizon

- Even if an investor invests in a mediocre fund or just an index for a long horizon, the returns would be good enough to meet the investment objective.

With ‘Patience’, you don’t need any financial knowledge to meet out the investment objectives. The ability to ‘sit tight’ is critical. (This does not mean that selecting better funds doesn’t have an impact)

Most personal finance advice is given out for capital gains, but inflation destroys most of the gains. I don’t think inflation is going to drop drastically anytime soon, which makes investing for capital gains less attractive. How would you suggest one starts investing for cash flow instead.

There seems to be some misunderstanding.

To beat inflation, investments must be made in avenues that yield higher returns than inflation. That’s the only solution.

What we forget while investing in Fixed Deposits, is that it gives us negative real returns (quite often). So say you did a FD @ 8.5%. On the 8.5% return than you got, if you paid 30% tax; your net return is only 5.95% which is below the inflation rate. This means after one year the net value of your money has reduced.

That’s why, exposure to equity as an asset class is very important. That’s where one can get the required capital gains over longer time horizons.

Say, if an investor’s retirement is 25 years from now, a significant portion of the retirement corpus must be invested in equity funds. Compounding in the right asset class shall work beautifully over long investment horizons.

Once a person has reached retirement, then he/she can invest for cash flows (using fixed maturity plans, short term debt funds etc.) which can keep generating returns and provide cash flows to meet out the expenses.

If you are asked to give advice to a 15 year old about investing. The goal is to retire with passive income by 30 years of age. What would your advice be?

With that goal in mind, here are the possibilities:

- Inherit wealth…!!!

- Be a very successful entrepreneur…!!!

I think it’s very difficult to ‘plan to retire’ at 30. Typically one would start earning by 22 and would only have 8 years to build a corpus that can last him/her for the next 50 years (assuming life expectancy of 80 years). It seems difficult until and unless there is something extra-ordinary.

May be the parent has to work extra hard for this to happen 🙂

How can one start to learn the basics of investing. What resources do you recommend?

I have found investopedia to be a very good resource. You can get a grasp of all the basic and advanced topics there. For a specific subject/topic; just google and you will find tons of material.

Jagoinvestor is a very good blog that you may also refer to.

Who is your favorite investor?

I love the way the earlier generation i.e. our parents used to save and invest.

They saved and invested consistently, right from their first salary cheque. Even with meagre incomes and low grade investment avenues like FDs and LIC policies, they made enough money to give us the best quality education, buy real estate, help their relatives and lead a decent lifestyle.

Compare it to youth today; even with much better salaries, our savings and investment habits are not that great and consistent.

Do you prefer technical or value investing?

Whatever makes money.

If someone can show me that he can make money via technicals, I would invest. I believe in the science of technical investing, high frequency trading etc., however that’s a special domain in itself.

Value investing again works but is not easy. Identifying the right stocks requires expertise.

For a common man, mutual funds is the way. Evaluate the experts, make your choice, trust them and sit tight.

What are your views on the efficient market hypothesis.

Some consultant sitting in the board meeting of a global bank might be on a call with his trader friend while we discuss the Efficient Market Hypothesis 😉

I don’t have the CV to challenge such a coveted theory, however, I have doubts on existence of a perfect world.

Consider the following:

- While some investors are pumping money in e-commerce, the experts call it a bubble. Similarly, stock prices move daily; even on days when there isn’t any stock specific information

- Is all information available to everyone at the same time? Perhaps No.

- Even with the same information, do we interpret it in the same way? No.

The theory may work when there is a human/automated way of processing the information in the same way by everyone, everytime and without emotions; given that the information is available.

Unfortunately, that may make the world boring too… 😉

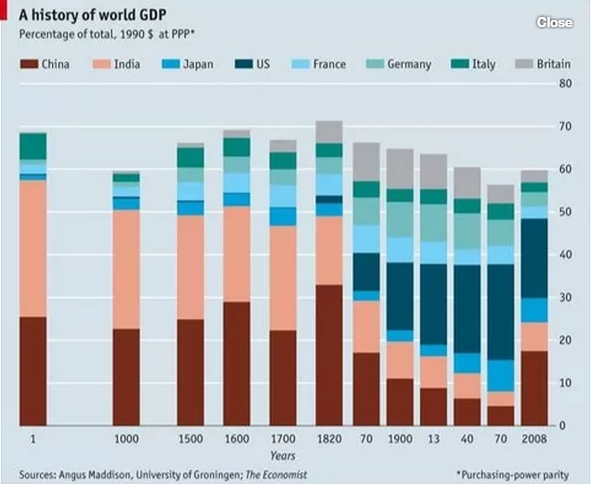

What are your views on the western world recovery? Do you buy it?

Look at the image below on GDP history of the world.

If India can go from one of the most prosperous countries at one time and then slide down to be an emerging economy and is again taking leaps to be an economic super-power; why can’t the western world go through the cycle.

Did I duck the question well enough? … 😉

Edit: Additional questions from Yuvraj (5-Jul-15)

I see all professional investment advisors preach and recommend mutual funds all the time. If in an hypothetical scenario, there were no mutual funds, how would you advice one to invest.

The logic behind preferring mutual funds is that you are hiring an expert to manage your investments.

If one can do better than fund managers then one can invest in stocks/bonds by himself. However, it’s worth noting that understanding markets and stocks is a full time job. So, one should weigh his/her expertise appropriately.

If the hypothetical scenario were true (say India in pre 80’s), the avenues available for asset allocation would be PPFs, gold, real estate, FDs etc. (The MF industry won’t be present only if the capital markets are in nascent stage).

If you could not invest in paper assets, where would you put your money?

At any point of time, one’s asset allocation would have exposure to hard assets like gold, real estate etc in an appropriate proportion. Though, even these hard assets can be purchased via paper assets like ETFs, REIT etc.

I can’t think of a real-world example one would not have any paper asset to invest. However, if it still happens and one has enough money then buy multiple properties and live on the rental income. It’s important to keep the debt-equity ratio favorable so that enough is left after debt servicing.

What are some strategies to safeguard a portfolio from a sudden decline in equities?

NONE.

We invest in equity knowing that it’s volatile and that’s why high returns. Money is made by ‘Spending time in the market and not Timing the market’.

A proper Asset Allocation ensures that you reach your investment goal after accounting for the volatilities inherent in the asset classes.

PS: My answers are for a normal investor.

Experts may try to work out PE strategies, Value-Investing etc. to gain from the declines. Let’s remember that we have our full time jobs and until and unless that’s in the finance zone, we shall be short of time to do such things effectively.

Are there ways to make money in the market is going down or sideways?

A normal investor shouldn’t worry about it.

Yes, there are professionals who do this. They study technical charts, price movements, take positions and make money with short term trading. The short term can be weeks, days, seconds and milli-seconds. There are many kinds of strategies including arbitrage strategies, pair trading, option strategies, HFT (High Frequency Trading) etc.

I want to clarify about investing for cash flow. I meant buying securities or assets that produce cash flow. The simplest example I can think of is rental properties. Why does no professional talk about investing for cash flow? Is passive income bad?

No income is bad.

There is no harm in rental income if one can have enough properties that fend for a person post retirement.

I don’t remember specifics, but I read a general rule about investing that says your age should determine the percentage of equity and debt in your portfolio. I think that’s poor advice, what do you think?

I agree. There can’t be a one-size-fit-all rule for everyone.

The rule says:

100 – Age = Proportion of your assets to be invested in stocks

It’s just a thumb rule that gives a starting point. The life expectancy is growing so people have amended it to say 110 – Age or 120 – Age. Besides, it also depends on an individual’s risk tolerance. Two people of same age might be comfortable with different asset allocation owing to their risk tolerance, lifestyle, earning etc.

Diversification vs focusing? Thoughts?

From mutual fund investor perspective

Some investors while buying mutual funds think of buying 2-3 schemes with different holdings. Essentially, they want to diversify.

However, what they miss is, if they invest in 2 large cap funds with different holdings they might end up being invested in the entire large cap stock universe (There are less than 100 large cap stocks in India). In such case, they may just get returns equivalent to the large cap index and the objective of investing in active funds gets defeated.

Asset allocation is good enough as a diversification measure for investors.

From stocks perspective

If I am able to pick stocks myself, then I would take concentrated positions because I would trust my ability. If I invest in multiple stocks, just to diversify, then somewhere I don’t trust my ability and in that case I shouldn’t pick stocks myself.

Diversification can turn to ‘diworsification’ easily, if investments are spread for wrong reasons.

Retire by 30

Great. Please do share the plan and how did you achieve it. It would add value to everyone.

Western World Recovery

Short term, they may have problems but the entire picture demands an extensive economic scrutiny, which is beyond this discussion.

The graph I have put forward is the economic cycle spanning centuries. We may not live to see what happens.

Do also note, how difficult it is for Greece to literally default; after theoretically defaulting 😉

Please feel free to comment, disagree and/or ask more…

Twitter: 3sharad

*****

You can ASK SHARAD any questions pertaining to Personal Finance or Investing!

*****

yuvraj wadhwani

I have some more now. 🙂

I see all professional investment advisors preach and recommend mutual funds all the time. If in an hypothetical scenario, there were no mutual funds, how would you advice one to invest.

If you could not invest in paper assets, where would you put your money?

What are some strategies to safeguard a portfolio from a sudden decline in equities?

Are there ways to make money in the market is going down or sideways?

I want to clarify about investing for cash flow. I meant buying securities or assests that produce cash flow. The simplest example I can think of is rental properties. Why does no professional talk about investing for cash flow? Is passive income bad?

I don’t remember specifics, but I read a general rule about investing that says your age should determine the percentage of equity and debt in your portfolio. I think thats poor advice, what do you think?

Diversification vs focusing? Thoughts?

You did duck the western world question well. Personally, I don’t buy it. Time will tell if I am right.

Personally, I think its a realistic goal to retire at 30. By retire I mean generate passive income to cover living expenses adjusting for inflation. I made a plan to retire by 30 and I may achieve it before 35 (fingers crossed). The plan is not selling my business btw. Im 29 now. I am fairly certain that I will if the macro economic scenario does nof change drastically.

asha chaudhry

yuvraj – pls comment this on ASK SHARAD post as well as we are trying to make that page a resource page. sharad too will comment at both places. many thanks for inspiring this post 🙂

Sharad Singh

Yuvraj. The new Q&A appended to the post.

Regards,

Sharad

Alok Rodinhood Kejriwal

Thank you for introducing me to this 2000 year chart!! LOVED IT!!

https://www.economist.com/blogs/graphicdetail/2012/06/mis-charting-economic-history

Sharad Singh

You have ‘the eye’ boss… !!!

Though the Economist’s chart is a better version (bar chart with spacing increments) of the area stacked chart, even that doesn’t bring out the key point mentioned in the article…

“The current hand-wringing over the ascent of Asia needs to be seen in historical context: as the restoration of Asian economic supremacy after a small blip…“

I have tried to put the graph with x-axis increments in 50 years (data sourced and approximated from the economist article/chart and interpolated) and the blip mentioned by Economist is visible on the right (18th century onwards).

Regards,

Sharad

Williambramb

dating websites new

[url=”http://datingonlinecome.com/?”]dating site reviews[/url]

Kevinsot

jewish gay dating in maine

gay gaming dating site

[url=”http://freegaychatnew.com?”]gay only web dating sites[/url]

Kevinsot

gay dating in a rural area

straight guy dating a gay guy

[url=”http://gaydatingzz.com?”]catholic gay dating[/url]

Kevinsot

black gay dating sites

dublin gay dating

[url=”http://freegaychatnew.com?”]cub gay dating[/url]