It has been a divided house on E Commerce Market Growth in India & also for future of E Commerce Companies. There have been statements on how E Commerce excluding travel (Etail) would become a 40 Billion USD market by 2020. The primary determinant of this has been attributed to growth of Internet penetration which is currently being & going to be driven by 3G & 4G on hand held devices. Statements have been made about how e commerce in India is where China was about a decade ago. All the latter could result in creation of minimum 8-10 companies having size of USD 5 billion & above. On the other hand there have been voice of concerns which speak about deep discounting being undertaken by the current etail players & which are burning cash for growth but profitability does not seem to be in sight. The war chest of cash created by them will help them grow but that may not lead to a sustainable business model as expressed by the naysayers.

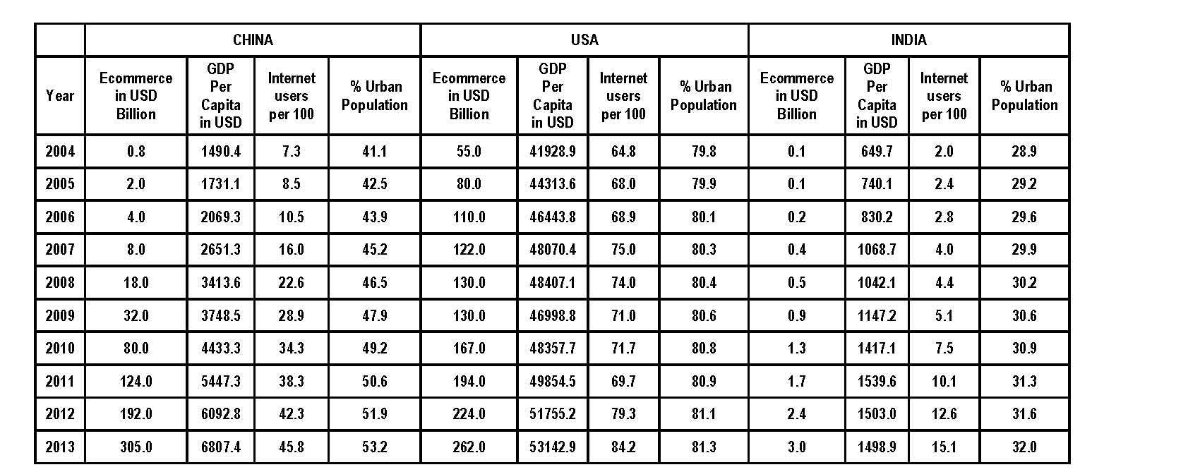

Below data represents the history & current state of E tail across China, USA & India with E tail (E Commerce without Travel) being the dependent variable & GDP per Capita, Internet Users & Urban Population being the Independent variables.

Note:

1)Ecommerce Size is only for Online Shopping by End Consumer excluding Travel

2) Sources – World bank and Multiple Sources

A small regression analysis run on the information point to some interesting results

- Urban Population is not a significant independent variable

- GDP Per Capita & Internet Users do influence dependent variable E Commerce

- None of the Countries exhibit behavior which can be strongly correlated with each other. They follow a different pattern

- Beyond a point, increased Internet Base hardly affects e commerce

- GDP Per Capita is a significant independent variable when compared to Internet Base

- The Inflexion Points which show quantum leap in US & China E Com Size are not fully explained by either GDP or Internet

- Projection for India does not translate into USD 40 Billion Market by 2020 assuming GDP growth rate of 8% & Internet Penetration of 40% population by 2020

Other Interesting Points to Note

- The Inflexion Points or Quantum Leaps are primarily on account of Independent Variables which today are not known or if known have not been fully quantified

- It is very possible that these Inflexion Points have to do with Cultural variables(Buying Behavior Individual as well as Group). China has a significant homogenous population.

- Other reasons also exist & one of them could be payment avenues. USA is a primarily Cards Driven Payments Market with China being a Non Cards but Payment Gateway (Ali pay, Ten Pay) driven E Commerce Market. India currently is a COD driven market. Chinese perception of Debt is completely different from American Perception of Debt. Hence the completely different payment means.

- Chinese E Commerce is more a market place driven Model Unlike USA & for that matter India which today looks like a Hybrid.

- Deep Discounting could be a primary reason for explosive growth seen in India in past 2 years primarily driven by bargain hunters & Novelty seekers

- The Product Categories amenable to E Commerce also don’t seem to be uniform in pecking order across the countries

- Indian Physical Infrastructure is way behind that of China & USA but smaller geography as compared to both may not be much of a deterrent.

- Chinese Market does not show evidence of deep discounting for growth & is profitable. US Market is skewed towards inventory liquidation & is more of the latter.

E Commerce is here to stay & will form a reasonable part of Retail Basket within India. Whether it touches 15% which China will or remains close to 5% which USA has cannot be predicted with any reasonable certainty for next 10 years. Brick & Mortar Models will undergo transformation but they have enough time on hand to reinvent their long term future. Prime Mover Advantage may not necessarily translate into being the dominant market share player after 10 years as Inflexion (Explosive Growth) may elude in first half of 10 years. It is possible that Slow & Steady in this case may win the race.

The Biggest Beneficiary here is going to be the Indian Customer at least for a reasonable time. Writing Obituary for E Commerce & Players in India is unwarranted but there is a need to rein in Euphoria Horses on the Extrapolated Potential as it is not going to touch 40 Billion USD by 2020

This is a reprint of my article published on linkedin

Alok Rodinhood Kejriwal

Very interesting. Are you a data scientist?

Can we meet? Please mail me at alok@rodinhood.com

Ravi Kumar

Dear Kalpesh,

Interesting, data backed analysis. As you have pointed out, it looks like GDP and Internet penetration have a big role to play – could it be their combination which drives the inflection point, say Per capita GDP crossing USD 4000 and internet penetration crossing 30%? Also, do you think the average age of the population might have some bearing on the growth of e-commerce? I am trying to come up with some cultural / behavioural pattern that might have an impact on the growth of e-commerce but can’t think of anything significant!

cheers

Ravi

KALPESH DESAI

Hi Ravi

I have tested the combined strength of these variables, there does not seem to any material change in results which can actually uphold statistically that combination of these two variables is responsible for inflexion point. As regards other demographic variables gender could result in a correlation but is unlikely to be an independent variable because it a well established fact in consumer buying as to which areas of a purchase decision men affect & which part of purchase decisions are influenced by women across many product categories. Since exact product category breakups are not known in terms of value, drawing statistical inference would be illogical.

Age would be variable but there is no data on age groupings & purchase value. % age group in a country population over a 10 year data period is not material enough for it to cause statistical significance as average would be 5 years over a 10 year date range.

If you were to look at NCAER data there are surprising results out there in terms of Indian consumer adoption for product categories & they do point to variables which are beyond demographics & income. One independent variable which i can think of is availability of information which has been increasing & perception about future deduced from this availability of information, which could be driving this adoption which is what i call non organic ( it does not follow a logical sequence or sequence seen in other countries). A similar story could have happened in US & China for those inflexion points. One would need to keep on testing the variables & retain them if statistically significant or dismiss them as mere co-relations.

Ravi Kumar

Thanks Kalpesh, for the detailed reply.

I am not sure information availability can be considered an independent variable as it is probably closely tied with the internet penetration %. I think more the penetration, more is the information availability.

Maybe a focus group can throw up some variables that we are missing which might actually shed some light on the inflection point. I am sure there is some factor that causes it – we just need to find it!

Thanks once again for your rigorous, data driven analysis.

Rishi

do you have the numbers for 2015?