When I heard that Flipkart had raised ANOTHER 200Mn US$ round in financing, my body went through hormonal changes. I was amazed at the strength of the Flipkart team and their business traction to raise such a massive sum; yet my calculative Marwari brain went a bit haywire.

I promised to write an UNBIASED view on the same, and while thinking of the approach remembered the Doodhwala (Milkman) who used to deliver milk at home. That bugger was a cunning guy – who would always “mix” pure milk with water; which made my Granny fret all day. In the end, he sold, we bought and what we drank was a heavenly mix of doodh and paani!

In this case, let me deliver the Flipkart funding story to you as reported in this media article and even separate the Doodh and the Paani (milk and water) for you. Then you decide what proportion of the story you want to buy!

Bansal said, “This investment validates the belief that our investors have, not only in our capabilities as a market leader, but also in the potential of e-commerce in India.”

Doodh part: There is no doubt that the existing/new investors of Flipkart have amazing faith in the existing team and hence have pumped in an additional 200Mn US$. No one manages to raise such large of amounts without ‘faith’. Bravo!

Paani part: I know of a very large Indian Industrial Group that had borrowed between 3-4 Billion US$ from ICICI, IDBI, etc in the mid 90s to build all kinds of ‘plants’ and ‘projects’ in India. The markets turned sour and the investors became cagey and very demanding. They refused to lend more monies to the promoters and demanded profitability from the projects, etc, etc.

One day, the promoter group CEO made a set of ‘mock keys’ and went to meet the investors. He told them, “Sorry, I am not able to run these businesses. Please take these keys of the plants and do as you please.”

The investors GOT THE MESSAGE. He was saying, “Either lend me more money or lose all the 3-4 Billion you have given me so far.” They lent more, and today that group is amongst India’s top 20!

I personally don’t know if the ‘existing’ investors of Flipkart are participating out of pain or pleasure. But given that Flipkart has already raised 180 million US$ in the past, investors are not really in a position to ‘write off the money’ as they would do if they would have invested 10-20 million US$ in small and medium companies.

Bansal: “We will use money to build the technology platform, further grow the supply chain besides talent acquisition.”

Doodh part: That sounds like a nice ‘PR’ statement, although I wonder why would ‘talent acquisition’ be mentioned here. I mean who raises 1200 crores in part to HIRE PEOPLE? Who the heck are these people? All the Fortune 500 CEOs???

Paani part: Let’s examine the current business of Flipkart. I see three companies in one:

– A courier company that only fulfills orders. This requires investments in warehouses, staff, vehicles, and yes, lots of technology to manage back-end. Let’s assume that the best business in this category is DHL.

– A Walmart-like purchase powerhouse that has the ability to BUY goods cheaply and then sell them expensively to consumers. The cheaper the purchase and more expensive the sale, the better the margins.

– A consumer Internet brand that has to grow popular each month and keep attracted to it by any means, with minimum advertising (advertising just for traffic becomes unviable). In this league, facebook and google come to mind. (A comScore Top India Internet sites chart is produced later).

So, in effect, Flipkart is going to try and become a better DHL, Walmart and Facebook all at once??

I think that is a really tough job!

Bansal said, “The company has already achieved half of its target of $1 billion GMV (Gross Merchant Volume) by 2015. We can be profitable even today if we want, but it is a strategic decision not to, as of now.”

Doodh part: It’s gratifying to know that at least the massive investments of the past (180 million = 1000 crores (excluding this one)) have at least resulted in a ‘break even business’!

Paani Part: ‘Just about profitable’ finds no meaning on any market of the world. You have to be Supercalifragilisticexpialidociously profitable to make any mark OR show some other promise to the market to be valued very high – as in the case MakeMyTrip who projects itself as the default leader of Travel in India/ (see MakeMyTrips market cap here despite it making a loss).

As per Bansal’s statement, as on today, Flipkart does 50% of 1 billion in GMV (Gross Merchandise Volume). That means that Flipkart does 500 million US$ = 3000 crores in Gross Revenues. If the company becomes ‘just profitable’ at this level of operations, let’s assume that the profit will be 5% = 150 crores = 25 million US$)

Now, check out this chart of market caps of ebay and Amazon – dated 13.07.13 and pay attention to the red arrows

Given the assumptions made on Bansal’s comments, in the USA stock markets, Flipkart would be valued best at 1.00 – 2.5 BN US$ (assuming 2-5x multiple on sales and/ or a 50-100x PE!)

Wow? Let’s consider the capital table of Flipkart post this round. Reports say that the VCs now own more than 50% of the Company.

Hence 380 million of investments have bought VCs 50% of Flipkart.

To get back a classic 10x on investment (=4 billion US$), Flipkart will have to sell or list at 7-8 BILLION US$ for its VCs to earn a 10x return on the same!!

(Side comment – even a 2.5 billion listing will result in VCs getting back 1.25 billion or 3-4x on their moneys. Nothing great in multiples, but definitely a BIG exit on a BIG investment and something that everyone would term a big success).

Bansal said, “The company has currently 9.6 million registered users and over 1 million unique visitors a day; it achieved a peak of 130,000 items shipped in a deal last month.”

Doodh part: 1 million daily unique visitors in India is GREAT. That’s no mean feat given that the top media Internet leaders are the usual biggies!

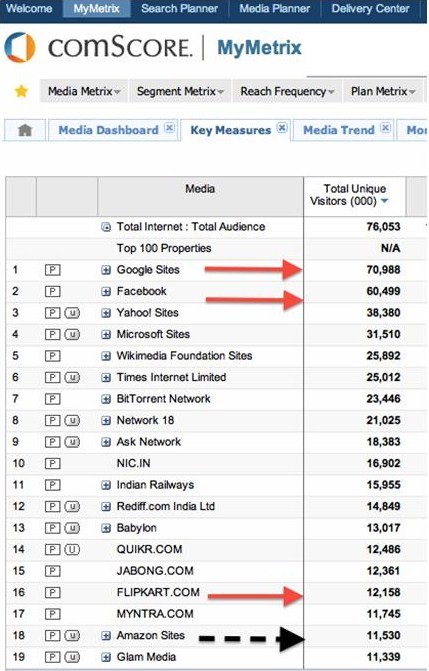

Check out this chart of Monthly Uniques of India (comScore May 2013)

Paani Part: CHECK OUT the AMAZON site’s traffic in India and how CLOSE it has crept up to Flipkart!

A haunting question I have is, “What is the COST of acquisition of the traffic of Flipkart?” If you look at the chart, Quikr.com is higher than Flipkart.com in May 2013. That is clearly from their relentless advertising. What would Flipkart’s traffic be without advertising?

Now, for the KILLER 🙂

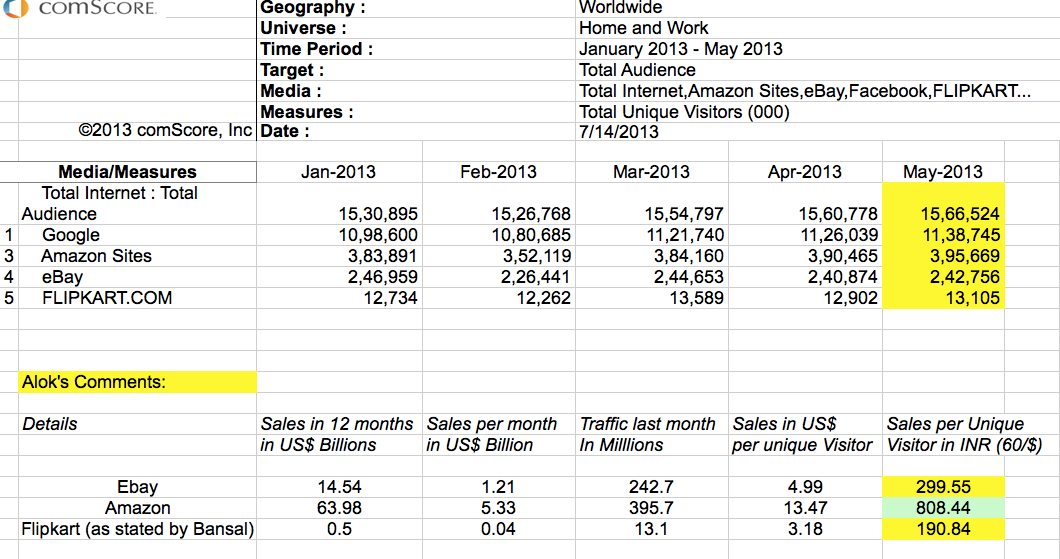

Check out THIS comScore traffic chart juxtaposed with the Market Cap data:

(note that the Internet traffic of Flipkart here is slightly higher since this is a global traffic chart):

The chart tells an interesting story…

Consider ARPUU’s (Average Revenue per Unique User):

Flipkart seems to be selling goods worth Rs. 190/- per unique visitor – a bit under ebay.com’s global ARPUU of Rs. 299/- ; BUT AMAZON ARPUU is a stratospheric Rs. 808/- per user!

If Flipkart has to become a Company double its size (1 billion US$ in revenues), it will have to double its traffic, which will then equal to the Times of India Group’s monthly traffic. To achieve this scale of traffic without expensive (and unprofitable) advertising will be very difficult. Else, it will HAVE TO INCREASE its ARPUU significantly.

Bansal: “This will not only enable us to reach our goal of $1 billion GMV by 2015 but also help us achieve bigger milestones in the future.” In April this year, the firm launched its marketplace and integrated it with its existing e-commerce platform to enable third party sellers to list and sell their products on its website and sell directly to consumers. The firm claims to have over 500 suppliers on the marketplace as of now.

Doodh part: Flipkart has done a GREAT job. They are the ‘e-commerce’ destination that every Indian I know uses and continues to use. Also, honestly, the brand is now so strongly entrenched, that it’s going to be difficult for the other ‘Chunnu Munnus’ of e-com in India to catch up. They will soon be cremated, buried or given to the birds (based on their preference).

Paani part: The challenge IS NOT FROM INDIA, BOSS!

IT’S FROM THIS MAMMONTH, GAMMOTH ANACONDA CALLED AMAZON!

This is the Corporate Vision of Amazon as it reads on their site. Just check its audacity: “We seek to be Earth’s most customer-centric company for four primary customer sets: consumers, sellers, enterprises, and content creators.”

!!!

If you get a few minutes, download and read this letter to shareholders Bezos wrote for 2012.

A few sentences to drive my later points:

– Prime Instant Video selection tripled in just over a year to more than 38,000 movies and TV episodes

– One industry observer recently received an automated email from us that said, “We noticed that you experienced poor video playback while watching the following rental on Amazon Video On Demand: Casablanca. We’re sorry for the inconvenience and have issued you a refund for the following amount: $2.99. We hope to see you again soon.” Surprised by the proactive refund, he ended up writing about the experience: “Amazon ‘noticed that I experienced poor video playback…’ And they decided to give me a refund because of that? Wow…Talk about putting customers first.”

– I am happy to report that I recently saw many Kindles in use at a Florida beach. There are five generations of Kindle, and I believe I saw every generation in use except for the first. Our business approach is to sell premium hardware at roughly break-even prices. We want to make money when people use our devices – not when people buy our devices. We think this aligns us better with customers. For example, we don’t need our customers to be on the upgrade treadmill. We can be very happy to see people still using four-year-old Kindles!

In 2013, Amazon is NOT the ‘e-commerce’ Company that Flipkart is trying to compete with (or will be forced to compete with)! That was the Amazon of 2005!!

Amazon TODAY is another PLANET.

Why do I say this?

Consider the points I mentioned about what comprises Flipkart – Courier & Logistics, Purchasing Power & Web presence & brand.

What comprises Amazon today?

Its CONTENT meets DEVICES meets DISTRIBUTION – all done seamlessly and as evident from anyone who has experienced Amazon before.

Amazon is the ONLY company that has succeeded in really successfully merging hardware (Kindle) and software (all kinds of content), beyond Apple Inc.

Jeff Bezos is NOT fighting the “Let me buy books cheap and then send them to Austin via my own expensive courier just to deliver it to Alokbhai there to make him happy.”

Nope. Bezos has MADE Alokbhai BUY a Kindle on which he BUYS books (that are severely discounted) and which INSTANTLY get delivered!! There is no blue dressed courier calling 10 times to find which galli Alokbhai lives in. No COD, no lafda, no problem.

Just before I end, let me quote a few lines from this epic article in Business Insider on Amazon and the Kindle:

- Amazon’s Kindle is no longer just a product: It’s a whole ecosystem.Specifically, it’s not just an e-book reader but a tablet, a media store, a platform for digital media sales, and even a publishing imprint.

- Media (means non physical stuff) is 45% of Amazon’s revenue, and it is in the midst of a secular disruption as physical media is replaced by digital media – (this tells you what the future is about!)

- Right now, Amazon generates 45% of its revenue from the sales of physical media–books printed on dead trees, DVDs and the likes. This form of media distribution is, slowly but surely, going the way of the dodo bird (or at least the tiger). No one knows when, no one knows how, but it’s happening.

- Amazon has to lead that disruption, instead of being disrupted by it. Books are a great example. With the original Kindle, Amazon pioneered the sale of digital books, and as a result owns over 90% of their distribution.

- Kindle is a decade-long investment in a media consumption and distribution ecosystem. It’s something Amazon can’t afford not to do because it needs to disrupt itself.

I am excluding all the existing business that Amazon does currently in India via its Market Place model of amazon.in (which Flipkart has also started). That’s all stupid distraction and will disappear when FDI is opened up, etc, etc.

I think the killer is going to be instant gratification of goods bought on platforms that are OPERATED BY e-commerce giants – NOT ‘via-via-via-via-via.’

Apple TV, Kindle and the Kindle App soon to be available on ALL Android Tabs and Phones in India is what will be Flipkart’s nightmare. That’s what they have to watch out for.

Can Flipkart create their own tab and platform like Amazon and iTunes/Apple?

Or most critically, as Business Insider puts it – Can Flipkart Disrupt itself when the time comes?!!

That my friend is the real adulterated question you need to separate into doodh and paani!

Your faithful doodhwala,

*****

Many thanks to Sumesh for the doodhwala image!!!