Is a startup on your mind?

After working for this large company for some years now, you are now feeling bored. It is not as exciting as it used to be, and you just hate the hierarchy.

Now, you want to start up on your own. You have thought of this great idea, which has been on your mind for some time. You can see the huge unmet demand in the market. The solution that you propose is going to be lapped up before it even hits the market. It’s the next multi-million dollar business. The press will be talking about it and your fellow peers will be going gaga (actually jealous).

I am sorry to break the bad news. That’s how the story starts in your mind. But that’s not how it moves forward.

It takes more than an idea to be an entrepreneur and to build a startup. The big question that you should be asking yourself is “Am I financially ready to start up?”

Having done 1 startup, moving into another and lived an almost a startup-like career, let me share with you my personal experience. A startup is not just all about fun. It is also a great struggle.

The idea of creating something that you believe in and taking it to the customers in the market is the fun part. However, a startup also tests you at every level – physical, mental, emotional and financial. It can be a great, perhaps the greatest struggle of your life.

I speak about this from personal experience of living an entrepreneur’s life and having gone through the grind.

The one thing that haunts you the most is money. And if you happen to be a family person – not being able to provide food on the kitchen table is the single biggest factor that can drive you to kill your startup dreams. Ask me!

Money, Money, Money

The fact is that you can handle a lot of pressures when you get your financials in place.

Hence, it is very important that before you start up, you have enough money to take care of at least the next 3 years of your personal expenses plus any expenses that you might need for your startup.

As you go through the initial and the most difficult phase of building your startup, it may involve multiple pivots to arrive at the right product-market fit. You will need enough financial backing to ride through this very demanding period.

Now, in all probability, you would say that you would get venture funding. You are right. You may.

Here’s the truth for you to consider. More than 95% of startup pitches are rejected. Mine was too!

While you hear a lot about startup funding and millions of dollars being offered even at idea stages, it does not mean that you too will find some God-sent Angels or Venture Capitalists to fund your startup dream. They may but only when they see that it makes profitable sense to do so.

The lesson is – Be prepared to do the journey yourself.

How much you may need will depend upon various factors? But I am going to make you a proposition. Here it is. You can save upto Rs. 83 lacs or over US Dollars 140,000 for your startup fund.

All this is your money. No VCs, no borrowings or no support from parents, friends, family. And here is the other better part. You can save all this money in less than 5 years.

Want to? Then, let’s go for it!

How to save Rs. 83 lacs or over 140,000 US Dollars for your startup dream

Let me reaffirm, this is absolutely possible. But let’s get one thing straight first.

Your COMMITMENT.

Would you keep your hand on any religious book that you believe in and say that “Nothing matters more to me than my startup“?

Only when you say a deeply resounding and confident “YES”, you may proceed further.

Do I hear a “Yes”? Great!

So this is what you have to do to fulfil your commitment.

SAVE MONEY LIKE MAD

Now I am not saying that you become a penny pincher and make one less trip to a weekend movie or reduce your eat outs. I actually want you to focus on some big money guzzlers that can stop you from making your dream come true.

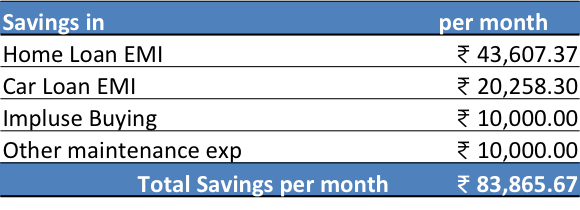

When you take care of these ‘big money guzzlers’, what do think could be your potential savings? My guess is that you can save upto a massive Rs. 84,000, per month.

Here’s a quick summary of where and how much.

Let’s understand this in some detail.

Caution: You will find that a lot of the ideas below are crazy. They are not what you would normally be advised to do, especially when you have a family. It is also very likely that when you tell your spouse, s/he is going to be totally mad at you. So, be prepared for the battle before the war!

Without further ado, here we go.

- Don’t buy a House. This is one of the most counter intuitive suggestions I am making.

- Don’t buy a Big Car – Is the newly launched Sedan on your mind?

- Avoid Impulse Purchases –

- BONUS – No Maintenance Costs – When you avoid that home and the big car, you also save yourself a heap of regular maintenance costs like property taxes, repairs, insurance, etc. All this can easily put back another Rs. 10,000 a month in your bank.

Together, all these add up to approximately Rs. 84,000 a month. Now, let’s say you have to pay a rent of Rs. 25,000 per month (since you don’t buy a house), you would still save Rs. 58,800 per month. No small number!

Additionally, you would also save on the downpayment (see assumptions below) of Rs. 16 lacs (Rs. 15 lacs for the house + Rs. 1 lac for the car). Wow!

The next step to your startup

But that’s not the end of story. It’s just the beginning. To build your startup fund, you need to take the next logical and critical step. That is invest the savings …bit by bit, month on month.

Now, if you invest this savings of Rs. 58,800 in a balanced portfolio of stocks, bonds and bank deposits, what would the result be?

For the purpose of illustration, let’s make our investment in a mutual fund, one of the easiest ways to invest your money. I will consider a balanced mutual fund which invests in government bonds, corporate bonds and stocks in a predefined ratio.

The fund that I have picked is one of the best performing mutual funds in the industry at reasonable risk and a great team managing it. The average returns of the fund for the past 3 and 5 years have been 21.5% and 14.3% respectively. (Based on values as on June 2, 2015)

Now, if you invest Rs. 58,800 per month for 5 years and it generates a return of 14.3% compounded yearly, then at the end of 5 years it would turn into Rs. 51.7 lacs.

Add to it the value of Rs. 16 lacs of the downpayment money, which is also invested in the same mutual fund. After 5 years, it would be worth Rs. 31 lacs.

In all, you would have close to Rs. 83 lacs at the end of 5 years.

If you can save more, you can have an even bigger startup fund.

Mission Accomplished! Take your money and go change the world.

It’s not easy – before or after

Let me remind you, it is not going to be easy. Our emotions have a strange way of fooling us. They stand between what we should be doing and what we end up doing. You need to really commit to your startup dream to make sure this happens.

Rome was not built in a day, nor your startup will be. Your startup fund will act as your lifeline in this long and arduous journey and enable you to pursue your dream of creating a long lasting business that you will be proud of.

Just one more thing on startups

Work on a real problem. Take up a pain points that bothers people so much that they would give you anything to solve it for them. After all, you want to make peoples’ lives better.

Let the money flow in but let there be more gratitude coming your way too. That would be a truly amazing story of your startup.

All the best!

—

A note on the assumptions: For the startup fund calculations , the following assumptions were made.

- You were to buy a house worth Rs. 50 lacs with a downpayment of 20% and a 10% legal and registration costs. You take a home loan for Rs. 40 lacs for a period of 20 years at an interest rate of 12%. The EMI for this would be Rs. 43,600.

- You were to buy a sedan which was to cost Rs. 10 lacs, all inclusive. You would take an auto loan of Rs. 9 lacs at 14% per year for a period of 5 years. The EMI for this would be Rs. 20,200.

- The maintenance costs of the above would be Rs. 10,000 per month.

- Your impulse purchases would average to about Rs. 10,000 per month.

—

This discussion originally appeared on www.vipinkhandelwal.com where Vipin writes on simple and actionable ideas on money and career. You can follow him on twitter @vipinkh.

*****

Liked this article?

Read ‘How to save an extra 25 lacs for your next startup’ by Vishal Khandelwal.

*****