Today we launched Tavaga on the Play Store. Please do download, give it a spin and let us know what you think!

Now onto the main post:

Two years ago, a bunch of us got together and decided to start-up, like a lot of folks around us (starting-up was the coolest thing to do back then!)

So we started with brainstorming on a few questions:

- What are we truly passionate about?

- What is it that we really want to do?

- How can we leverage our backgrounds?

- What did the successful startups do to get there?

- What is the one core value we need to deliver to our customer?

After some back and forth we found our answers. We all had a strong background in finance, and were all quite passionate about it. The most successful start-ups like Uber and AirBnB offer a value to their customers that was much needed. The value proposition of these companies is so strong that their customers are willing to actively help these companies challenge regulators.

If so, what is the value that Tavaga should deliver to its customers?

Simplicity!

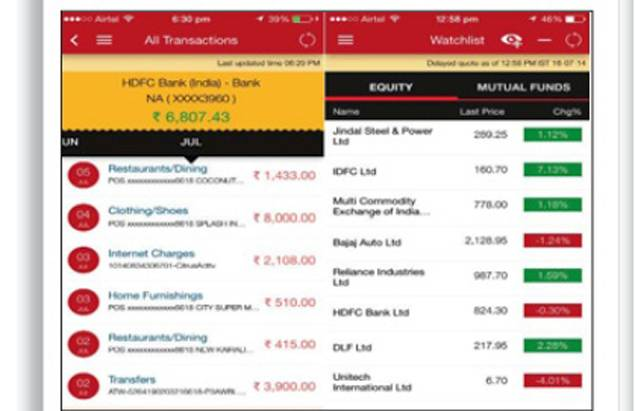

The world of finance is very complex, and when it comes to investing even more so. There are ‘market experts’ with half baked knowledge of finance, who keep puking names of stocks day in and day out on business news channels. They lace their speeches with a healthy dose of complex jargon to ensure they come across as experts. There is no way for normal people like us to figure out if they are any good at picking stocks.

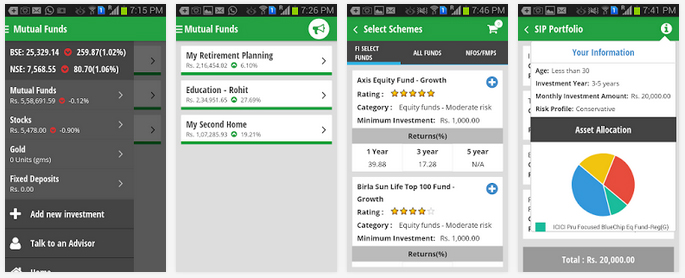

Then there are ‘investment advisors’ running around with forms, and pitching funds with complex names like IXIXI Smart ABC XYZ Fund — Growth Option — Regular Plan. No one knows what that means, how it works or how it is going to help them reach their financial goals. You are told these are the best 2 or 3 of the 10,000 funds out there, and that you won’t be able to buy a house or send your child to a good college if you didn’t put all your money into this fund immediately. To prove the point, they will then inundate you with numbers and complex jargon that you don’t understand. None of this makes sense to anyone, but for the fear of losing out, we all give in and sign the papers.

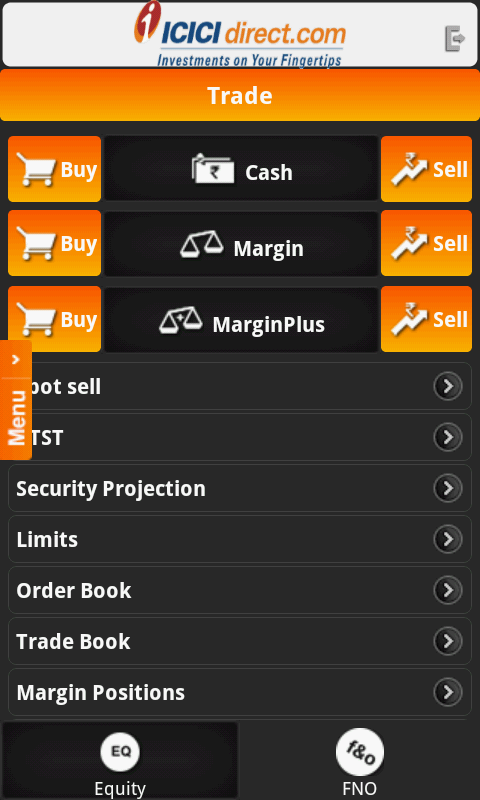

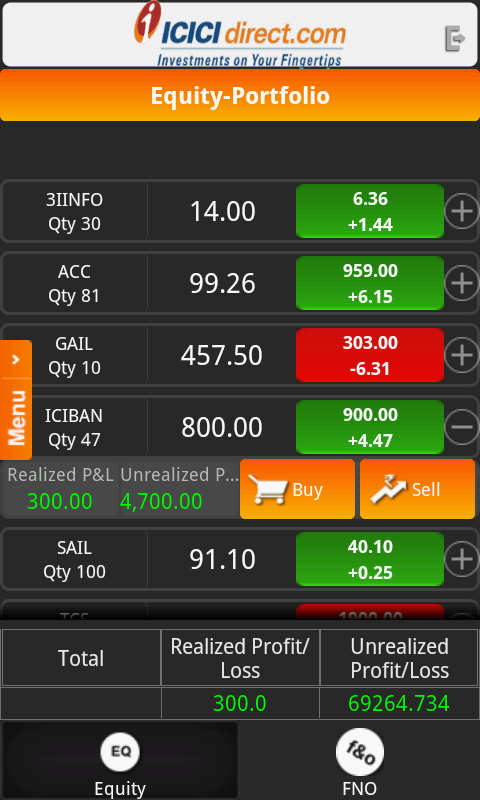

Do their apps do a better job? Not really. They are all just an app version of the same service — too many numbers, too much jargon, too much text — just too many things!

What the customer desperately needs is simplicity — numbers they understand, words they can relate to and most importantly, to feel that they are in control of their future, not the scary folks I described above.

And so Tavaga was born, with one value proposition:

‘Invest Simply!’

However, delivering simplicity is not easy. As we researched, we realised that the whole process is very complex from a customer perspective. They don’t know what they are buying, they don’t know if it is suitable for their needs, and they don’t know how to link these investments to their actual goals.

Typically the seller, be it a bank representative or a financial advisor, starts with pitching a fund to the customer. After either greed or fear sets in, customers are presented with a bunch of forms. One of them being a risk assessment questionnaire. This paper has questions like ‘What will you do if the markets fall by 20%?’, with options like — ‘stay invested, buy more, sell’. That gets the customer thinking — Wait a minute, didn’t the guy just say that this fund is going to go up by 20%? Why am I being asked about markets falling? What would I really do? I have no idea what I would do, because I was thinking only about the fund going up by 20% and what I’d do with the profit. What can I do with a loss?’. After 2 or 3 such questions, the customer just gives up, looks for the signature box and lets the agent fill in the rest of the form.

And then, a year later when the profit is nowhere close to the promised 20%, a different guy from the same bank shows up, tells you that the other guy was dumb and that he will move your money to the fund that ranked No. 1 last year. You are then left wondering if you are any closer to buying that house today than you were last year.

Delivering Simplicity!

Solving these problems was not simple. The questions in the risk assessment questionnaire are important, and we do need to understand the customer’s willingness to take risk. After that, we need to find a way to let the customer focus on what matters to them the most — their goals.

We set out to find a way to get our customers to answer the same questions without really answering any of those questions. Confusing?

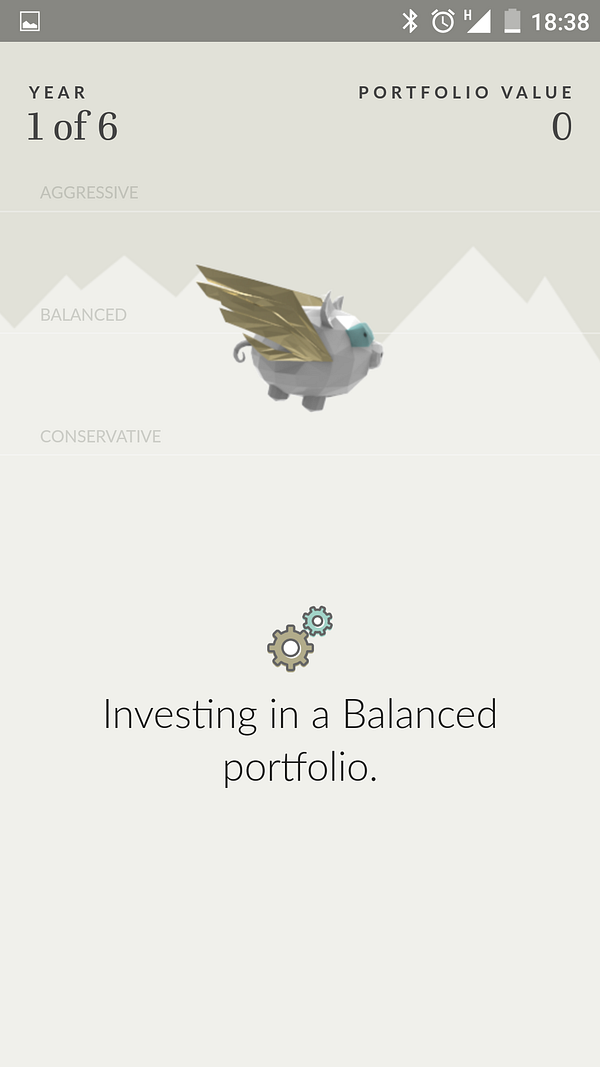

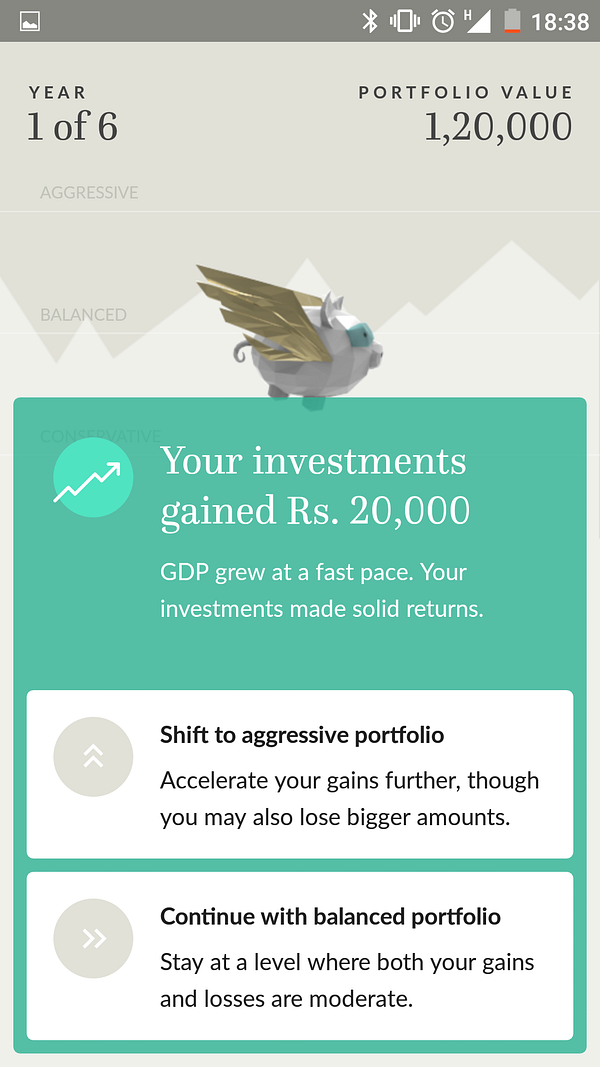

Enter the ‘Investor Attitude’ simulation.

We created a simple simulation game where the customer starts with a portfolio worth Rs. 1 lakh, and decides to increase or reduce the risk depending on the outcome of the simulation. This simulation runs for 6 periods and based on the decisions made by the customer, we deduce the answers to the same questions as in a questionnaire.

The customer is not bombarded with complex jargon, yet we get all the answers we want. And that’s how we simplified risk profiling!

Then we had to figure out how to keep the customers focused on their goals, and not the names of the funds or the numbers they churn out every day.

How did we do that?

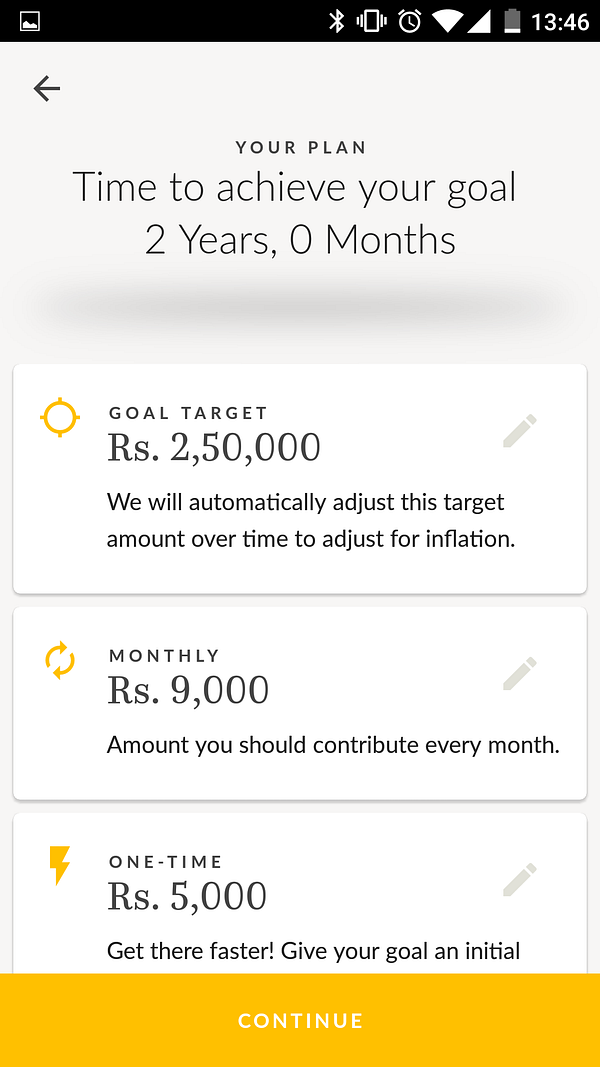

Step 1 — Create a simple interface for customers to tell us what they are saving for.

We built a simple flow where the customer inputs what their goal is, how much will it cost them and when they want to achieve the goal. Based on this input, we create a simple goal plan that tells them how much they need to save every month to reach their goal. If they think it is too high or low, they can always tweak it.

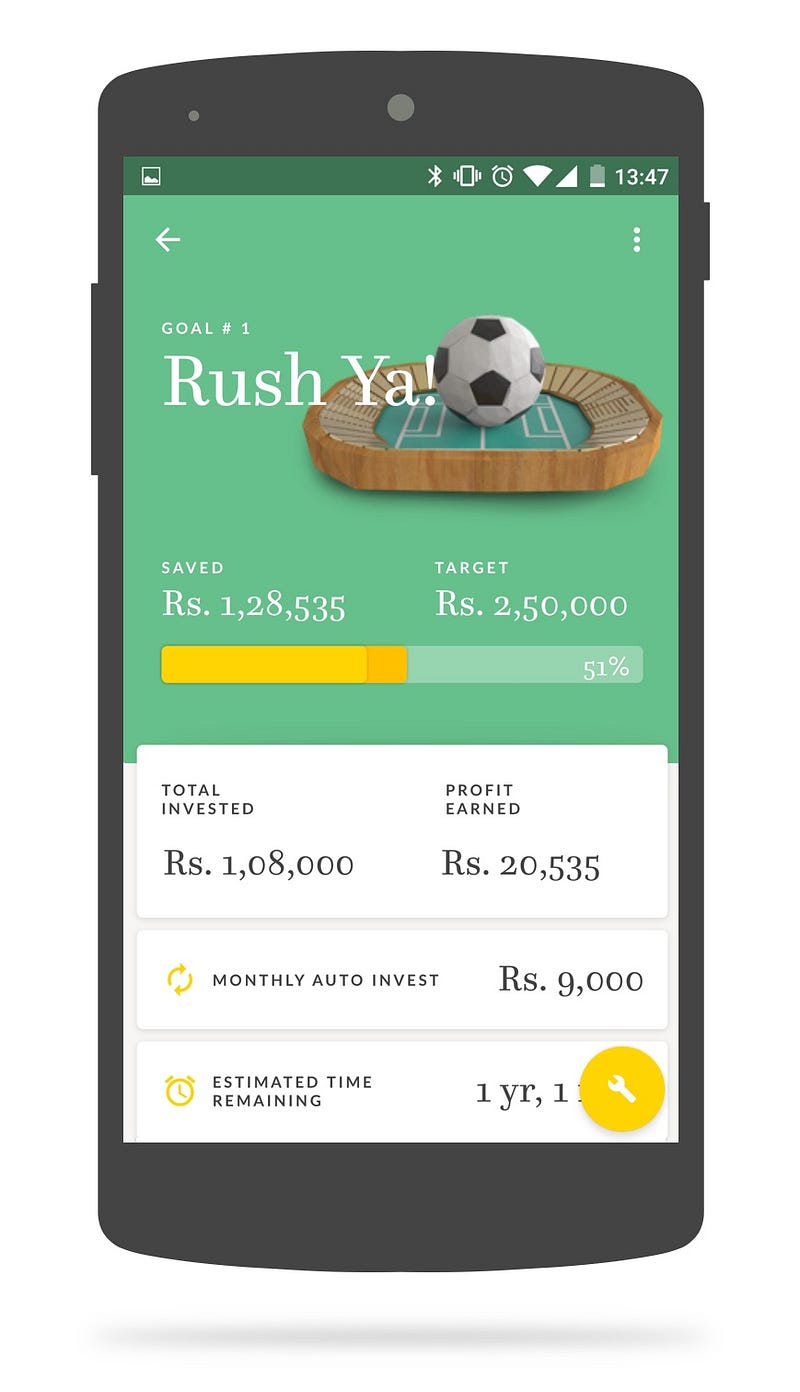

Step 2 — A goal dashboard.

When a customer opens the app, they don’t see funds and daily movements. They see their goals. They see how much they have invested towards a goal, how much of the target is completed, and how far they are from reaching their target. Do you really need to know anything more than this about your goals? We believe most people want to know just that much, and that is exactly what we show.

Delivering this simplicity didn’t come cheap. We spent a lot of time brainstorming, building prototypes, showing them to customers, going back to the drawing board, and repeating the whole process several times, before we had what we believed was simple enough.

Everything we built goes against conventional wisdom. Several industry experts wrote us off even before they saw the product. One particular “very reputed veteran” of this industry said that there are at least 500 really good ideas waiting to happen in fintech, and this definitely is not one of them. He recommended we shut down and go back to our jobs.

The time has finally come when customers will judge who’s right and who’s wrong 🙂

If you have read through till here, you’re clearly interested in the product. I would urge you to first download a few other apps like an ICICI or a ShareKhan, and then download Tavaga to experience the full impact of the simplicity. Once you give Tavaga a spin, do let us know what you think of it!