My kid was turning 3 in a few days and we had planned a family get together. My parents had come over for the birthday and my in-laws were arriving that day.

Over lunch, the conversation meandered from my work to my dad’s post retirement life to my kid’s school admissions. (School admissions in Mumbai are no less difficult than cracking IITs/IIMs. The latter might be a tad easier.)

Amidst the talk, my father declared (my father normally doesn’t suggest, he declares) that he would gift my kid a FD (Fixed Deposit) to fund his education. While I suggested he should use his savings to go on a leisure world trip, he in his typical don’t-tell-me tone said “I have enough money for myself. My insurance policy is maturing next month and I shall gift that to my grandson.”

I curiously asked “which policy”?

He proudly stated “I started this policy when you were studying engineering. The policy provided life cover till maturity and a sum assured payable on maturity.”

“When you had a horizon of 18 years, why didn’t you invest in mutual funds?” I asked.

“Huh… Does your mutual fund give me insurance and the returns too?” he retorted.

“Wait.” I said.

I opened my laptop and quickly worked out some numbers in excel with the details my father gave me about the policy. In a few minutes, my answer was ready.

I said “Wouldn’t it have been better if you got 2.5 times the money that you are getting from your policy?”

He had been expecting an answer all the while, but this literally took him by surprise.

“WHAT THE HELL?” he exclaimed. “Are you kidding?”

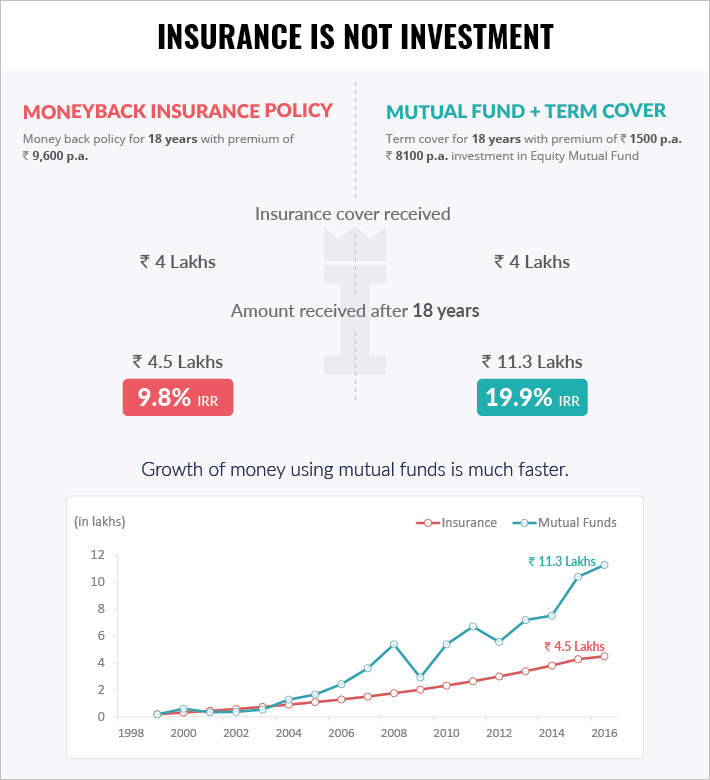

I explained him the concept as in illustration above (numbers used are sample but not misleading)

- Out of the 9600 that you invested every year, you got an insurance cover for 4 Lakh and sum assured on maturity equal to 4.5 Lakh

- The investments could have been alternatively done as following:

- Purchase a pure term cover of 4L for Rs. 1500 p.a.

- Invest remaining 8100 p.a. into mutual funds

Had he invested as in the second option, he would have been indifferent in terms of insurance, however, he would have had 2.5 times the money he would currently have.

Rather than 4.5L that the insurance policy is paying on maturity, investment in mutual funds would have given him 11.3L.

He murmured “Wow, that kind of thing would have even funded the Ivy league education for my grandson…”

The entrepreneur in me said “… or seed-funded his venture… who knows… “.

I noticed, my wife signaling something. It was time to pick-up my in-laws from the airport.

I pushed off to the airport, thinking – what gift is my father-in law getting?

Would it be deja-vu with another WT’X’ moment?

This article was originally published at Invezta

asha chaudhry

SHARAD!!!!

what a delightful, easy to comprehend read this was!

omg – even for someone like me who hates to talk financial figures and details (much to alok’s delight :)))) I COULD UNDERSTAND AND ENJOY READING THIS!!

more power to inveszta and the writer in you. pls always strive to write in this style ‘coz simple is what defines you as a great writer!

Sharad Singh

Hi Asha,

Thanks for the encouraging words. They shall motivate to continue meeting the expectations… 🙂

PS: Though Shakespeare once said “What’s in a name”, but in the digital world it can lead to 404 error. The name is Invezta 🙂

Regards,

Sharad

asha chaudhry

my bad sharad 🙁

i just multitask all the time – so am bound to misspell something – as long as i tweet it correctly (already followed INVEZTA as soon as this post was approved) i’m sure we’ll be cool 🙂

Sharad Singh

Hey… don’t mind. I just took the opportunity to plant a back-link 🙂

Thanks for the follow and the consistent support… 🙂

Regards,

Sharad

Vishwajeet

Thank you so much for writing this. This proved my idea of Investment vs Life Insurance. 🙂

Sharad Singh

🙂

Someone pointed… “Insurance is for death. Investment is for life.”…!!!

KALPESH DESAI

Hi Sharad

What you have shown is a very generous plan for insurance ( :

A good way to Nudge customer to a taking a rational financial decision

LIC which sells such traditional plans now account for only 50% of new individual premiums. Group schemes, they are still large. This is likely to decline as is evident from drop from 70% a few years ago.

The point being customers are getting aware of what you have pointed out. Obviously there is a switch to a better products like ULIP’s from money back or fixed/bonus plans

I think the fundamental comparison here should be between ULIP & Term +MF.

From a pure cost perspective ULIP will not win at current cost structure but i see that IRDA has been clamping on cost over past 10 years. From 45% commission on first year premiums with obnoxious premium allocation & admin charge when they started it is down by 40% in 10 years.

As on date ULIP is still a loser on cost but if past trend is to go by there may be surprises in store & consolidation in insurance space may bring about this very soon.

ULIP is sold as long term product 15-20 years (return plus life). MF as a product with long term which was 3 years in 2000 & post Lehman is 5-7 years as on date.

The MF fund manager is under pressure to deliver every quarter or he risks losing AUM as the investors/advisers/distributors are savvy. The below proves the point.

If one looks at the new money which has flown into MF’s in past 2 years & in particular this year with Gross Sales of 8000 cr per month, i dont see the same funds which attracted money pre Lehman at the forefront.

The ULIP fund manager at best is being evaluated every 10 years by the person buying the ULIP which allows fund manager to pick value stocks thus there is an inherent window available for fund manager to outperform. Thus he may outperform a MF fund manager but only time will tell.

Churning MF once every 2 years to beat such risk on returns posed on account of Q to Q performance may be a good strategy but a customer would see this a ploy of adviser to charge fees or in case of distributor, commission taking into account his perception of investment time frame.

Human minds don’t like complexity. Ulips purely from a human mind perspective are less complex than Term plan plus MF.

This avoidance of complexity in a human mind creates compartments. Investment compartment is not the same as Life Risk mitigation compartment & that is not same as Retirement compartment.

A Proper & Repeated “Nudge” is what can break this compartments & it has to done fast before ULIP’s get their act together. Financial Decisions are not rational & that’s why there is a complete science of Behavioral Finance dedicated to it.

There is a large market who can Nudged away to MF Plus Term & let us hope that the time window available (ULIP’s not getting their act together) will remain as wide as now to break the compartments in human mind.

This will allow people to make right financial decisions.

Ps

Why don’t you put up a IRR comparison of lowest cost ULIP (Point to Point returns) with Term plan taken before 10 years plus Point to Point Return of BSE (this will be like a no churn MF) over past 10 years. It will be an interesting result to see purely from difference in IRR.

Sharad Singh

Wow Kalpesh. Thanks for the detailed note.

My primary objective of the post is to “AWAKEN”. That’s why a “generic” insurance plan. Yes, I welcome the comparison with other insurance options; shall do that sometime.

ULIP is a bigger sin. Investors haven’t been sold ULIPs or insurance for simplicity. They have been MIS-SOLD.

If regulator can turn things around, it would be good for everyone.

Yes, ULIP is (mis)sold as a long term product but when a person realises what he has bought, he doesn’t have a way out 🙂 (If one withdraws before 3 years, you hardly get your principal back…!!!)

In my opinion, patience with mutual funds is the best way to generate wealth. Of course, one can mess even with Aces on hand.

Regards,

Sharad