Part 1: Demystifying employee equity — The Basics.

Important: Equity compensation and the actual value of equity (i.e. how and when it translates to money in your hand) is governed by individual investment contracts, how your company structures its dealings during capital infusion, and taxation. What I talk about below barely scratches the surface i.e. it only tries to answer the very basic questions. The calculations are based on the generic startup employee who joins after some funding has been received, unless otherwise mentioned.

So you just killed your interviews at that fancy new startup, and now it’s time for the $ negotiations. This is what the founder writes on piece of paper and hands to you.

‘200k + 0.1% equity’

Before you start rubbing your hands in glee at becoming part owner of the next unicorn, let’s get this straight as a general rule.

You are not going to make money off your equity in a startup.

Why?

- 90% of all startups fail.

- If you’re in the small % of companies who IPO, the lifetime of a startup to IPO is long. Alibaba was founded in 1999, and IPO’ed in 2015. Uber was founded in 2009, and is still a couple of years from IPO. So expect anything between 5–10 years for you to cash out, if at all.

- Even on IPO, how much you make depends on a large number of factors: at what stage you joined, how much investment the company takes in the future, and of course the final valuation of the company on exit. Read this: Big IPO, tiny payout.

Let’s talk about what the equity you are being offered means.

0.1% equity does not mean:

- That you own 0.1% of the company from the day you join.

- That you own 0.1% of the company when you leave.

At the stage you come in, let’s assume the company is owned by founders and investors. Typically out of the 100% of the company, 15–20% will be set aside as the equity compensation pool for employees, with the rest owned by founders and investors according to the investment terms. It is from this pool that your equity as an employee is granted.

Now comes the next important bit — the difference between equity and ESOPs (or employee stock options).

Employee Stock Options

The 0.1% equity which is offered to you is not really shares in the company. What you own is actually an option to buy 0.1% of the company. (It’s quite literally an option, you can choose not to buy the shares). So how do you make money off equity if it’s just an option to buy the shares, and you don’t really own them?

Option Math

Here’s how you make money of your options. If you own an option, this is what it will say: “This contract gives you the right to buy shares of company X at 2$ per share at any date in the future.” Now if at any date in the future the share is valued at 20$, then use the option (the technical term is exercising the option) buy the share for 2$, sell it at 20$ and pocket the 18$ (minus taxes). Note: The founders already paid the money to buy their shares when they incorporated the company, which is why they own direct equity and not options. So they get to sell the shares at 20$ and keep all the 20$.

Where did the price of 2$ (the price at which you buy the share using the option) come from?

This is usually based on the valuation of the company at the time you join. If you’re offered 1,000 shares out of a total of 1,000,000 (equal to 0.1% of the company) and the company is valued at 2 million dollars, then each share is worth 2 dollars. The price of the option i.e. the price at which you have the right to buy shares at a later date, is usually the same as that of the share price of the company, in this case 2$.

Vesting:

Why should the founders give you even an option to buy 0.1% of the company at the date you join without you paying anything for it?

The short answer is that they don’t. You are paying for your share of the company through your hard work, and possibly a cut in salary. Since your work will only start yielding benefits some time down the line, it is only logical that your ownership is also cascaded accordingly. This is done through vesting. The 0.1% ESOPs offered to you typically vest over 4 years with a one 1 year cliff i.e your 0.1% is prorated over 4 years, with the first accrual happening after you complete one year with the company. The remaining 3/4th of your ESOPs can vest at any time period (daily/weekly/monthly/yearly etc) depending on your arrangement with your employer. Vesting sounds harsh, but it makes sense and everybody including founders’ equity is vested using the same rules.

Dilution

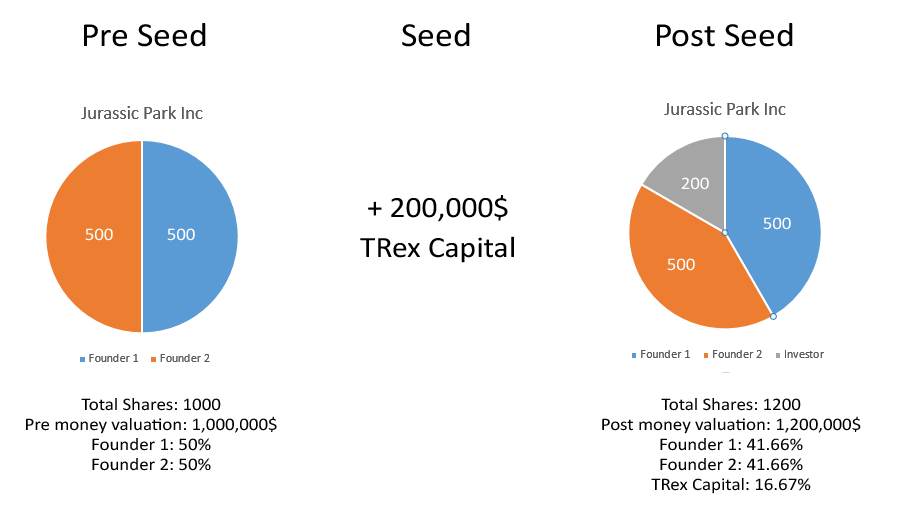

Dilution implies that every time a part of the company is sold off (to investors), your share (in terms of % of the company) decreases. Let’s take an example.

Jurassic Park Inc is started with the aim of recreating dinosaurs. The two founders incorporate the company with 1000 shares (500 shares each). At a seed funding round by TRex Capital, they raise 200,000$ at a valuation of 1 million dollars (this is called the pre money valuation i.e. valuation before the seed round). Each of the 1000 shares of the company are worth 1,000,000/1,000 = 1000$ per share before the infusion of the 200k. The company’s valuation post funding is 1m+200k (from the seed investor) =1.2 million dollars.

Now how many shares does the investor own? If he invests 200k, and each share was worth 1000$, he owns 200 shares. Where did these new 200 shares come from? These are newly created and issued to the investor, so the total shares of Jurassic Park Inc available are now 1000 (owned by the founders) + 200 (owned by TRex Capital, the investors) = 1200. Earlier a 1000 shares made up 100% of the company. Now 1200 shares make up 100%. So it’s obvious that the percentage holding of each stakeholder goes down. This is dilution.

By how much? In the post funding scenario, each founder has 500 shares which is 500/1200 = 41.67% of the company, and the investor has the remaining 200/1200 = 16.66% of the company.(41.67+41.67+16.66=100%).

In summary, at every funding round (when new shares are created and sold to investors, the % of the company you own decreases, but the total number of shares you own remains the same. So if you owned 500 shares (50%) worth 1000 each at Series A, and at Series B your holding is diluted to 41.67%, each of your shares would be valued higher. This is because investors typically pay more money for a lesser portion of the company as it grows, which means the valuation of the company, and therefore the price of each share, increases.

The dilution logic applies equally to everyone who owns equity/ESOPs in the company.

Let’s take a real world example (We’ll leave out dilution). Jim joins Scooby Doo Corp as a Growth Engineer, and he is offered 0.5% of ESOPs — 4 year vesting and 1 year cliff. Jim has read this article and understands that he needs to know what that 0.5% is worth today (i.e. the valuation of the company.) Turns out the valuation is 5 million dollars, so Jim’s 0.5% is worth 25,000$ today. He also finds out that 0.5% is 500 shares (the total number of shares of Scooby Doo Corp is 100,000), which means each share today is worth 50$. He confirms with his employer that this is the price he can buy the share at once it vests.

2 years later, Jim leaves the company to start his own adventure sports business. He now owns 0.25% of the company vested over 2 years (assuming there was no further investment and hence no dilution of his holding), worth 12,500$. In another 2 years, the company gets acquired by Dastardly Villains Inc. for 20 million $. Jim does some quick math in his head. Somebody is paying 20m $ for all 100,000 shares of Scooby Doo Corp, which means each share will be bought at a price of 200$. Jim exercises his options, buys the shares at 12,500$ (at 50$ per share) and sells it for 50,000$ (at 200$ per share) to Dastardly Villains Inc.. Ka-ching!

Note: Jim can sell his shares because there is somebody acquiring the company and willing to pay Jim in cash. This is called a liquidation event, when shares can be converted into cash either through an acquisition or through an IPO.

Hope this helps some of you who are looking to move to startups and are confused about how the equity compensation works.

TLDR: You should join a startup for the learning curve and NOT for the money/equity.

PS: Here are some more resources for those interested.

How I negotiated my startup compensation

Joining an early stage startup?

Quora – How much equity should a non founding employee ask for?

How to think about cash vs equity compensation

I’m @mythun on Twitter and share content about startups, product, and design.

First published on the Cubeit Blog.

****

Recommended reads on trh on the topic: ESOPs for Startups

The Basics of Equity, Stakes & Shares for Startup Entrepreneurs

Co-founder Percentages – Key to a Successful Venture

Basic Funding Concepts for Entrepreneurs

*****

asha chaudhry

hey mithun,

i’m not allowed to have faves – but you are soon becoming one of my favorite writers on trh!!!

this is really useful – a lot folks post queries on esops and equity and your post is refreshingly simple to understand!!

also read abhishek’s post and alok’s comment – https://www.therodinhoods.com/forum/topics/co-founder-percentages-key-to…

this is an interesting ppt alok has created to for folks who don’t understand basic funding concepts 🙂

https://www.therodinhoods.com/forum/topics/basic-funding-concepts-for-en…

and of course – esops for startups – another simplified ppt alok has created

https://www.therodinhoods.com/forum/topics/esops-for-startups-by-rodinhood

asha chaudhry

ps: i love the jurassic park inc example :))))))

pps: some folks have got rich – but yes, it’s nice to keep everyone grounded and aware of reality 🙂

Mithun Madhusudan

Thanks for the complement Asha!

Went through the posts above. Very informative! Allocating equity among ‘founders’ when they don’t know each other is a problem that has to be tackled very discreetly, and love the quantitative way the post has broken down both issues.

asha chaudhry

hey mithun,

don’t know how i forgot this one!

https://www.therodinhoods.com/forum/topics/the-basics-of-equity-stakes-shares-for-startup-entrepreneurs

Mithun Madhusudan

this is great! will take quite a few tips from this for my next post 🙂

Varun Chawla

Hey Mithun,

Very interesting and informative read. Does clear up a lot of basics. Another resource which I think will be useful for folks interested in start up finance and startups in general could be Paul Graham’s essays (https://www.paulgraham.com/articles.html)

Mithun Madhusudan

Thanks for the feedback Varun! I’ve gone through quite a few of the essays by Paul Graham and they’re well put together. Can’t say the same for some of his recent work though, especially the one about income (in)equality by startups. Went a little overboard there.

asha chaudhry

hey mithun,

this might interest you as well (yeah alok’s written extensively on the topic!)

https://www.therodinhoods.com/forum/topics/the-mystery-of-entrepreneur-salaries

Mithun Madhusudan

As usual Alok has hit the nail on the head! Salaries MUST be taken by entrepreneurs (of course at a reasonable level). They have too much to worry about in terms of running and growing the business to have to additionally worry about whether they can pay rent the next month. It’s just an unnecessary source of distraction

Alok Rodinhood Kejriwal

Its a nice catchy topic but really not always true.

The most important reason missed by you is that there is now a vibrant secondary market of high quality startups that may be created by the venture itself or by investors punting. This is how Twitter, FB etc enriched lots of employees even before they hit IPO. Also the same I hear with Flipkart.

Mithun Madhusudan

Still a minuscule number Alok. The point of the title was to drive home the point that as an employee you shouldn’t consider giving up cash for equity unless you are into it for the long term and are really invested in the company.

Deeti Dave

I was listening to someone’s interview y’day, and something he said has to do with your title here, hence, thought of mentioning here.

Statistically, more than 80% of the start-up founders do not get even close to being millionaires. The reason they still continue to start up is, the freedom of doing what they really enjoy, at their own terms without being accountable to anyone, and still make enough money to survive. 🙂

Mithun Madhusudan

Exactly! You should never never never go in for the money. Find another reason 🙂